VII. Securitisation

I. Introduction

1.In December 2014, the Basel Committee on Banking Supervision (BCBS) published a revised framework for calculating bank capital requirements for securitisation exposures, with further revisions in July 2016. The revised securitisation framework aimed to address a number of shortcomings in the Basel II securitisation framework and to strengthen the capital standards for securitisation exposures held in the banking book. The Central Bank’s Standards on Required Capital for Securitisation Exposures is based closely on the BCBS framework.

2.A central feature of the revised framework is a hierarchy of approaches to risk-weighted asset calculations. The BCBS framework includes approaches based on internal credit risk ratings of banks. These approaches have not been included in the Central Bank’s Standards, as internal ratings-based approaches are not deemed appropriate for use in capital calculations at this time by banks in the UAE.

3.Consequently, the hierarchy of approaches within the Central Bank’s Standards begins with the revised External Ratings-Based Approach (SEC-ERBA), and below that in the hierarchy the revised Standardised Approach (SEC-SA). For resecuritisations, the hierarchy excludes the SEC-ERBA, and instead begins with the SEC-SA. If neither the SEC-ERBA nor the SEC-SA can be applied for a particular securitisation exposure, a maximum risk weight of 1250% must be used for the exposure.

4.Calculations under both the SEC-ERBA and the SEC-SA depend to some degree on a measure of “tranche thickness.” The thickness of a tranche is determined by the size of the tranche relative to the entire securitisation transaction. In general, for a given attachment point, a thinner tranche is riskier than a thicker tranche, and therefore warrants a higher risk weight for risk-based capital adequacy purposes. While credit rating agencies capture some aspects of the risk related to tranche thickness in their external ratings, analysis performed by the BCBS suggested that capital requirements for a given rating of a mezzanine tranche should differ significantly based on tranche thickness, and this is reflected in the Standards.

5.Under the SEC-ERBA, risk weights also are adjusted to reflect tranche maturity. The BCBS incorporated a maturity adjustment to reflect unexpected losses appropriately in the capital calculations. External ratings used for SEC-ERBA typically reflect expected credit loss rates, and the BCBS concluded through analysis during the development process that the mapping between these expected losses and unexpected losses (the quantity that capital is intended to cover) depends on maturity.

II. Clarifications

1. Securitisation

6. The Standards defines a securitisation as a contractual structure under which the cash flow from an underlying pool of exposures is used to service claims with at least two different stratified risk positions or tranches reflecting different degrees of credit risk. The creation of distinct tranches is the key feature of securitisation; similar structures that merely “pass through” the cash flows to the claims without modification are not considered securitisations.

7. For securitisation exposures, payments to the investors depend upon the performance of the specified underlying exposures, as opposed to being derived from an obligation of the entity originating those exposures. The stratified/tranched structures that characterize securitisations differ from ordinary senior/subordinated debt instruments in that junior securitisation tranches can absorb losses without interrupting contractual payments to more senior tranches, whereas subordination in a senior/subordinated debt structure is a matter of priority of rights to the proceeds of a liquidation.

8. In some cases, transactions that have some of the features of securitisations should not be treated as such for capital purposes. For example, transactions involving cash flows from real estate (e.g., in the form of rents) may be considered specialized lending exposures. Banks should consult with Central Bank when there is uncertainty about whether a given transaction should be considered a securitisation.

2. Senior Securitisation Exposures

9. A securitisation exposure is considered a senior exposure if it is effectively backed or secured by a first claim on the entire amount of the assets in the underlying securitised pool.

10. While this generally includes only the most senior position within a securitisation tranche, in some instances there may be other claims that, in a technical sense, may be more senior in the waterfall (e.g., a swap claim) but may be disregarded for the purpose of determining which positions are treated as senior.

11. If a senior tranche is retranched or partially hedged (i.e., not on a pro rata basis), only the new senior part would be treated as senior for capital purposes.

12. In some cases, several senior tranches of different maturities may share pro rata in loss allocation. In that case, the seniority of these tranches is unaffected – they all are considered to be senior – since they all benefit from the same level of credit enhancement. (Note that in this case, the material effects of differing tranche maturities are captured by maturity adjustments to the risk weights assigned to the securitisation exposures, per the Standards.)

13. In a traditional securitisation where all tranches above the first-loss piece are rated, the most highly rated position should be treated as a senior tranche. When there are several tranches that share the same rating, only the most senior tranche in the cash flow waterfall should be treated as senior (unless the only difference among them is the effective maturity). In addition, when the different ratings of several senior tranches only result from a difference in maturity, all of these tranches should be treated as senior.

14. In a typical synthetic securitisation, an unrated tranche can be treated as a senior tranche provided that all of the conditions for inferring a rating from a lower tranche that meets the definition of a senior tranche are fulfilled.

15. Usually, a liquidity facility supporting an ABCP program would not be the most senior position within the program; instead, the commercial paper issued by the program, which benefits from the liquidity support, typically would be the most senior position. However, when a liquidity facility that is sized to cover all of the outstanding commercial paper and other senior debt supported by the pool is structured so that no cash flows from the underlying pool can be transferred to other creditors until any liquidity draws are repaid in full, the liquidity facility can be treated as a senior exposure. Otherwise, if these conditions are not satisfied, or if for other reasons the liquidity facility constitutes a mezzanine position in economic substance rather than a senior position in the underlying pool, the liquidity facility should be treated as a non-senior exposure.

3. Operational Requirements for the Recognition of Risk Transference

16. The Standards requires that banks obtain a legal opinion to confirm true sale to demonstrate that the transferor does not maintain effective or indirect control over the transferred exposures and that the exposures are legally isolated from the transferor in such a way (e.g., through the sale of assets or through sub-participation) that the exposures are put beyond the reach of the transferor and its creditors, even in bankruptcy or receivership. However, that legal opinion need not be limited to legal advice from qualified external legal counsel; it may be in the form of written advice from in-house lawyers.

17. For synthetic securitisations, risk transference through instruments such as credit derivatives may be recognized only if the instruments used to transfer credit risk do not contain terms or conditions that limit the amount of credit risk transferred. Examples of terms or conditions that would violate this requirement include the following:

(a) Clauses that materially limit the credit protection or credit risk transference, such as an early amortization provision in a securitisation of revolving credit facilities that effectively subordinates the bank’s interest, significant materiality thresholds below which credit protection is deemed not to be triggered even if a credit event occurs, or clauses that allow for the termination of the protection due to deterioration in the credit quality of the underlying exposures. (b) Clauses that require the originating bank to alter the underlying exposures to improve the pool’s average credit quality. (c) Clauses that increase the bank’s cost of credit protection in response to deterioration in the pool’s quality. (d) Clauses that increase the yield payable to parties other than the originating bank, such as investors and third-party providers of credit enhancements, in response to a deterioration in the credit quality of the reference pool. (e) Clauses that provide for increases in a retained first-loss position or credit enhancement provided by the originating bank after the transaction’s inception. 4. Due Diligence

18. The Standards requires banks to have a thorough understanding of all structural features of a securitisation transaction that would materially affect the performance of the bank’s exposures to the transaction. Common structural features that are particularly relevant include those related to the payment waterfall incorporated in the structure, which is the description of the order of payment for the securitisation, under which higher-tier tranches receive principal and interest first, before lower-tier tranches are paid. Credit enhancements and liquidity enhancements also are important structural features; these may take the form of cash advance facilities, letters of credit, guarantees, or credit derivatives, among others. Effective due diligence also should consider unusual or unique aspects of a particular securitisation structure, such as the specific nature of the conditions that would constitute default under the structure.

5. Treatment of Securitisation Exposures

1. Risk Weights for Off-Balance-Sheet Exposures

19. The Standards requires that banks apply a 100% CCF to any securitisation-related off-balance-sheet exposures that are not credit risk mitigants. One example of such an off-balance-sheet exposure that may arise with securitisations is a commitment for servicer cash advances, under which a servicer enters into a contract to advance cash to ensure an uninterrupted flow of payments to investors. The BCBS securitisation framework provides national discretion to permit the undrawn portion of servicer cash advances that are unconditionally cancellable without prior notice to receive the CCF for unconditionally cancellable. The Central Bank has chosen not to adopt this discretionary treatment, and instead requires a 100% CCF for all off-balance-sheet exposures, including undrawn servicer cash advances.

2. Adjustment of Risk-Weights for Overlapping Exposures

20.Banks may adjust risk weights for overlapping exposures. An exposure A overlaps another exposure B if in all circumstances the bank can avoid any loss on exposure B by fulfilling its obligations with respect to exposure A. For example, if a bank holds notes as an investor but provides full credit support to those notes, its full credit support obligation precludes any loss from its exposure to the notes. If a bank can verify that fulfilling its obligations with respect to exposure A will preclude a loss from its exposure to B under any circumstance, the bank does not need to calculate risk-weighted assets for its exposure B.

21.To demonstrate an overlap, a bank may, for the purposes of calculating capital requirements, split or expand its exposures. That is, splitting exposures into portions that overlap with another exposure held by the bank and other portions that do not overlap, or expanding exposures by assuming for capital purposes that obligations with respect to one of the overlapping exposures are larger than those established contractually. The latter could be done, for instance, by expanding either the assumed extent of the obligation, or the trigger events to exercise the facility. A bank may also recognize overlap between exposures in the trading book and securitisation exposures in the banking book, provided that the bank is able to calculate and compare the capital charges for the relevant exposures.

3. External Ratings-Based Approach (SEC-ERBA)

22. To be eligible for use in the securitisation framework, the external credit assessment must take into account and reflect the entire amount of credit risk exposure the bank has with regard to all payments owed to it. For example, if a bank is owed both principal and interest, the assessment must fully take into account and reflect the credit risk associated with timely repayment of both principal and interest.

23. A bank is not permitted to use any external credit assessment for risk-weighting purposes where the assessment is at least partly based on unfunded support provided by the bank itself. For example, if a bank buys ABCP where it provides an unfunded securitisation exposure extended to the ABCP program (e.g., liquidity facility or credit enhancement), and that exposure plays a role in determining the credit assessment on the ABCP, the bank must treat the ABCP as if it were not rated. The bank also must hold capital against the liquidity facility and/or credit enhancement as a securitisation exposure.

24. External credit assessments used for the SEC-ERBA must be from an eligible external credit assessment institution (ECAI) as recognized by the Central Bank in accordance with the Central Bank standards on rating agency recognition. However, the securitisation Standards additionally requires that the credit assessment, procedures, methodologies, assumptions and the key elements underlying the assessments must be publicly available, on a non-selective basis and free of charge. Consequently, ratings that are made available only to the parties to a transaction do not satisfy this requirement. Where the eligible credit assessment is not publicly available free of charge, the ECAI should provide an adequate justification, within its own publicly available code of conduct, in accordance with the “comply or explain” nature of the International Organization of Securities Commissions’ Code of Conduct Fundamentals for Credit Rating Agencies.

25. Under the Standards, a bank may infer a rating for an unrated position from an externally rated “reference exposure” for purposes of the SEC-ERBA provided that the reference securitisation exposure ranks pari passu or is subordinate in all respects to the unrated securitisation exposure. Credit enhancements, if any, must be taken into account when assessing the relative subordination of the unrated exposure and the reference securitisation exposure. For example, if the reference securitisation exposure benefits from any third-party guarantees or other credit enhancements that are not available to the unrated exposure, then the latter may not be assigned an inferred rating based on the reference securitisation exposure.

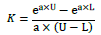

4. Standardised Approach (SEC-SA)

26. The supervisory formula used for the calculations within the SEC-SA has been calibrated by the BCBS to generate required capital under an assumed minimum 8% risk-based capital ratio. As a result, the appropriate conversion to risk-weighted assets for the SEC-SA generally requires multiplication of the computed capital ratio by a factor of 12.5 (the reciprocal of 8%) to produce the risk weight used within broader calculations of risk-based capital adequacy. This multiplication by 12.5 is reflected in the requirements as articulated in the Central Bank’s Securitisation Standards.

27. If the underlying pool of exposures receives a risk weight of 1250%, then paragraph 5 of the Introduction of the Standards for Capital Adequacy of banks in the UAE is applicable.

28. When applying the supervisory formula for the SEC-SA to structures involving an SPE, all of the SPE’s exposures related to the securitisation are to be treated as exposures in the pool. In particular, in the case of swaps other than credit derivatives, the exposure should include the positive current market value times the risk weight of the swap provider. However, under the Standards, a bank can exclude the exposures of the SPE from the pool for capital calculation purposes if the bank can demonstrate that the risk does not affect its particular securitisation exposure or that the risk is immaterial, for example because it has been mitigated. Certain market practices may eliminate or at least significantly reduce the potential risk from a default of a swap provider. Examples of such features could be:

• cash collateralization of the market value in combination with an agreement of prompt additional payments in case of an increase of the market value of the swap; or

• minimum credit quality of the swap provider with the obligation to post collateral or present an alternative swap provider without any costs for the SPE in the event of a credit deterioration on the part of the original swap provider. If the bank is able to demonstrate that the risk is mitigated in this way, and that the exposures do not contribute materially to the risks faced by the bank as a holder of the securitisation exposure, the bank may exclude these exposures from the KSA calculation.

6. Treatment of Credit Risk Mitigation for Securitisation Exposures

1. Tranched Protection

29.In the case of tranched credit protection, the original securitisation tranche should be decomposed into protected and unprotected sub-tranches. However, this decomposition is a theoretical construction, and should not be viewed as creating a new securitisation transaction. Similarly, the resulting sub- tranches should not be considered resecuritisations solely due to the presence of the credit protection.

30.For a bank using the SEC-ERBA for the original securitisation exposure, the bank should use the risk weight of the original securitisation for the sub-tranche of highest priority. Note that the term “sub-tranche of highest priority” only describes the relative priority of the decomposed tranche. The calculation of the risk weight of each sub-tranche is independent from the question of whether the sub-tranche is protected (i.e., risk is taken by the protection provider) or is unprotected (i.e., risk is taken by the protection buyer).

2. Maturity Mismatches

31.For synthetic securitisations, maturity mismatches may arise when protection is bought on securitised assets (when, for example, a bank uses credit derivatives to transfer part or all of the credit risk of a specific pool of assets to third parties). When the credit derivatives unwind, the transaction will terminate. This implies that the effective maturity of all the tranches of the synthetic securitisation may differ from that of the underlying exposures.

7. Simple, Transparent, and Comparable Criteria

32. In general, to qualify for treatment as simple, transparent, and comparable (STC), a securitisation must meet all of the criteria specified in the Standards, including the Appendix to the Standards. The criteria include a requirement that the aggregated value of all exposures to a single obligor as of the acquisition date not exceed 2% of the aggregated outstanding exposure value of all exposures in the securitisation. However, the BCBS has permitted flexibility for jurisdictions with structurally concentrated corporate loan markets. In those cases, for corporate exposures only, the applicable maximum concentration threshold for STC treatment can be increased to 3%. This increase is subject to ex ante supervisory approval, and banks with such exposures should consult with the Central Bank regarding STC treatment. In addition, the seller or sponsor of such a pool must retain subordinated positions that provide loss-absorbing credit enhancement covering at least the first 10% of losses. These credit-enhancing positions retained by the sellers or sponsor are not eligible for STC capital treatment.

III. Example Calculations

A. Standardised Approach

33.Consider a bank applying the SEC-SA to a securitisation exposure for which the underlying pool of assets has a required capital ratio of 9% under the standardised approach to credit risk. Suppose that the delinquency rate is unknown for 1% of the exposures in the underlying pool, but for the remaining 99% of the pool the delinquency rate is known to be 6%. The bank holds an investment of 100 million in a tranche that has an attachment point of 5% and a detachment point of 25%. Finally, assume that the pool does not itself contain any securitisation exposures, so the exposure is not a resecuritisation.

34.In this example, KSA is given at 9%. To adjust for the known delinquency rate on the pooled assets, the bank computes an adjusted capital ratio:

(1 − W) × KSA + (W × 0.5) = 0.94 × 0.09 + 0.06 × 0.5 = 0.1146

35.This calculated capital ratio must be further adjusted for the fact that the delinquency rate is unknown for a small portion (1%) of the underlying asset pool:

KA = 0.99 × 0.1146 + 0.01 = 0.1235

36.Next, the bank applies the supervisory formula to calculate the capital required per unit of securitisation exposure, using the values of the attachment point A, the detachment point D, the calculated value of KA, and the appropriate value of the supervisory parameter ρ, and noting that D>KA:

where:

Note that because this is not a resecuritisation exposure, the appropriate value of the supervisory calibration parameter rho is 1 (ρ=1).

37.Substituting the values of a, U, and L into the supervisory formula gives:

38.This tranche represents a case in which the attachment point A is less than KA but the detachment point D is greater than KA. Thus, according to the Standards, the risk weight for the bank’s exposure is calculated as a weighted average of 12.5 and 12.5×K:

39.With a tranche risk weight of 954%, the bank’s risk-weighted asset amount for this securitisation would be 954% of the 100 million investment, or 954 million. If, for example, the bank chose to apply a capital ratio of 13% to this exposure, then the bank’s required capital would be 13% of 954 million, or approximately 85 million, on the investment of 100 million in this securitisation tranche.

B. External Ratings-Based Approach

40. Consider a non-senior securitisation tranche that has been assigned a rating by one of the eligible rating agencies corresponding to a rating of BB+. Suppose that the tranche has an attachment point A of 5%, a detachment point D of 30%, and effective tranche maturity of MT = 2 years.

• From the look-up table for SEC-ERBA, a non-senior securitisation exposure rated BB+ with one-year maturity has a risk weight of 470%; the risk weight for a five-year maturity is 580%.

• The tranche maturity of 2 years is one-quarter of the way between one year and five years, so the relevant maturity-adjusted risk weight based on linear interpolation is one quarter of the way between 470% and 580%, or 497.5%.

• Because this is a non-senior tranche, it must also be adjusted for tranche thickness, which is the difference between D=30% and A=5%, a difference of 25%. The interpolated risk weight from the table should be multiplied by a factor of 1-(D-A)=0.75, which exceeds the floor of 50% and therefore should be used by the bank in the calculation (0.75 x 497.5%).

• The resulting tranche risk weight is 373%.

41. Banks using the SEC-ERBA for securitisation exposures may prefer to incorporate the main features of the ERBA look-up tables into formal calculations of risk weights, including the relevant adjustments for tranche maturity and tranche thickness. In that case, each pair of 1-year and 5-year risk weights can be viewed as coefficients for a formulaic calculation of the risk weight for a tranche of given maturity MT, and in the case of non-senior tranches, thickness D-A.

42. For example, for a non-senior tranche rated BB+ with MT between one year and five years, the tranche risk weight RWT can be computed with a single formula as:

where the coefficients 4.7 and 5.8 correspond to the relevant values from the look-up table of 470% for one-year maturity and 580% for five-year maturity. Substituting in the values for A, D, and MT from the example above:

43. Senior tranches are not adjusted for thickness; hence, the calculation of the tranche risk weight RWT for a senior BB+ rated tranche would be computed as:

where again the coefficients 1.4 and 1.6 correspond to the relevant values from the senior tranche columns of the look-up table, specifically 140% for 1-year maturity and 160% for 5-year maturity.