Guidance for Capital Adequacy of Banks in the UAE

C 52/2017 GUI Effective from 1/4/2021Introduction and Scope

This document articulates all guidance that have been drafted for banks in the UAE with regards to capital.

The Guidance is based closely on requirements of the framework for capital adequacy developed by the Basel Committee on Banking Supervision.

This Guidance should be read in conjunction with the associated Standards issued by the Central Bank (Standards for Capital Adequacy of Banks in the UAE - October 2019).

Pillar 1

I. Tier Capital Supply

Introduction

This guidance explains how banks can comply with the Tier Capital Supply Standard. It must be read in conjunction with the Capital Regulation and Standards for Capital Adequacy of Banks in the UAE. Guidance regarding Minimum Capital Requirement and Capital buffer as stated in the document have to be followed by all banks for the purpose of regulatory compliance.

1.To help and ensure a consistent and transparent implementation of Capital supply standards, Central Bank will review and update this guidance document periodically.

2.The guidance document has structured into six main sections

- 1. Scope of Application

- 2. Eligible capital

- 3. Regulatory adjustments

- 4. Threshold deductions

- 5. Significant investment in commercial entities

- 6. Frequently Asked Questions

1. Scope of Application

3.“Financial activities” do not include insurance activities and “financial entities” do not include insurance entities.

4.Examples of the types of activities that financial entities might be involved in include financial leasing, issuing credit cards, portfolio management, investment advisory, custodial and safekeeping services and other similar activities that are ancillary to the business of banking

Treatment of investment in Insurance Entities

5.Insurance subsidiaries are to be deconsolidated for regulatory capital purposes (i.e. all equity, assets, liabilities and third-party capital investments in such insurance entities are to be removed from the bank’s balance sheet) and the book value of the investment in the subsidiary is to be included in the aggregate investments.

6.Investments in the capital of insurance entities where the bank owns more than 10% of the insurance entity’s common share capital will be subject to the “Threshold deductions” treatment. Amounts below the threshold that are not deducted are to be risk weighted at 250 %.

(Investments in insurance entities wherein ownership is greater than 10% will also include insurance subsidiaries)

2. Eligible Capital

Accumulated Other Comprehensive Income and Other Disclosed Reserve

7.For unrealized fair value reserves relating to financial instruments to be included in CET1 capital banks and their auditor must only recognize such gains or losses that are prudently valued and independently verifiable (e.g. by reference to market prices). Prior prudent valuations, and the independent verification thereof, are mandatory.

8.The amount of cumulative unrealized losses arising from the changes in fair value of financial instruments, including loans/financing and receivables, classified as “available-for-sale” shall be fully deducted in the calculation of CET1 Capital.

9.Revaluation reserves or cumulative unrealized gains shall be added to CET 1 with a haircut of 55%.

10.The amount of cumulative unrealized gains arising from the changes in the fair value or revaluation of bank’s own premises and real estate investment are not allowed to be included as part of Asset Revaluation reserve for regulatory purposes.

11.IFRS9 will be implemented during 2018. Banks that are impacted significantly from the implementation of IFRS9 may approach the Central Bank to apply for a transition period for the IFRS9 impact. Such applications will be analysed and considered on a case-by-case basis.

Retained Earnings

12. The amount reported under accumulated retained earnings (5.1.4.1) should be as per the audited financial statement at year end and should remain the same for the entire financial year.

13. Current financial year’s/quarter’s profits can only be taken into account after they are properly audited/ reviewed by the external auditors of the bank. Current financial years /quarter’s loss if incurred have to be deducted from the capital.

14. Dividend expected/ proposed for the financial year should be reported under (5.1.4.3) and will be deducted from Retained Earnings/ (Loss) (5.1.4). Expected dividend applies only for Q4 until dividend is actually paid.

15. The dividend deduction must be updated based on each of the following events, if the amount changes, after Annual General meeting, or the approval from the Central Bank, or the release of the Financial Statements by the auditors.

16. Other adjustments to the Retained Earnings includes: a. Prudential filter: Partial addback of ECL in accordance with the Regulation Regarding Accounting Provisions and Capital Requirements - Transitional Arrangements should be reported under (5.1.4.4) IFRS transitional arrangement.

b. CBUAE Regulatory deductions: i. Amount exceeding Large Exposure threshold: Any amount that is in violation of Large Exposure regulation of notice 300/2013 shall be deducted from the capital. Any amount deducted from CET1 under 5.1.4.5 of the BRF 95 due to a Large Exposure violation of notice no.226/2018 may be excluded for the calculation of risk weighted assets. However, amounts that are not deducted must be included in risk weighted assets. Furthermore, any counterparty credit risk (under CR2a) associated with such exposure must remain included in the calculation of risk weighted asset.

ii. Loans to directors: The circular 83/2019 on Corporate Governance regulations for Banks, under the article (6) “Transaction with Related parties” requires if the transaction with the related parties are not provided on arm’s length basis, then on general or case by case basis, deduct such exposure from capital. The deduction should be reported under 5.1.4.5 of the BRF 95. Capital Buffers - Countercyclical Buffer

17.The buffer for internationally active banks will be a weighted average of the buffers deployed across all the jurisdictions to which it has credit exposures. The buffer that will apply to each bank will reflect the geographic composition of its portfolio of credit exposures. When considering the jurisdiction to which a private sector credit exposure relates, banks should use, where possible, an ultimate risk basis; i.e. it should use the country where the guarantor of the exposure resides, not where the exposure has been booked.

18.Banks will have to look at the geographic location of their private sector credit exposures (including non-bank financial sector exposures) and calculate their countercyclical capital buffer requirement as a weighted average of the buffers that are being applied in jurisdictions to which they have an exposure. Credit exposures in this case include all private sector credit exposures that attract a credit risk capital charge or the risk weighted equivalent trading book capital charges for specific risk and securitisation.

19.The weighting applied to the buffer in place in each jurisdiction will be the bank’s total credit risk charge that relates to private sector credit exposures in that jurisdiction, divided by the bank’s total credit risk charge that relates to private sector credit exposures across all jurisdictions. Banks must determine whether the ultimate counterparty is a private sector exposure, as well as the location of the “ultimate risk”, to the extent possible.

20.The charge for the relevant portfolio should be allocated to the geographic regions of the constituents of the portfolio by calculating the proportion of the portfolio’s total credit exposure arising from credit exposure to counterparties in each geographic region.

Please refer to Question 15 of the FAQs below for further guidance and examples of countercyclical buffers.

3. Regulatory Adjustments

Goodwill and Other Intangibles

21.Intangible assets typically do not generate any cash flows and hence their value, when a bank is in need of immediate additional capital to absorb losses, is uncertain. For this reason, all intangible assets are deducted from CET1 (5.1.8.1).

22.From regulatory perspective, goodwill and intangible assets have the same meaning as under IFRS.

23.Capitalized software costs that is not “integral to hardware” is to be treated as an intangible asset and software that is “integral to hardware” is to be treated as property, plant and equipment (i.e. as a fixed asset).

24.The amount of intangible assets to be deducted should be net of any associated deferred tax liability (DTL) that would be extinguished if the asset became impaired or derecognised under the applicable accounting standards.

25.Goodwill and intangible assets that are deducted from CET1, they are excluded from the calculation of RWA for credit risk exposure value.

Deferred Tax Assets

26. Deferred tax assets (DTAs) typically arise when a bank:

- suffers a net loss in a financial year and is permitted to carry forward this loss to offset future profits when calculating its tax bill (net losses carried forward)

- has to reduce the value of an asset on the balance sheet, but this 'loss in value' is not recognised by the tax authorities until a future period (temporary timing difference)

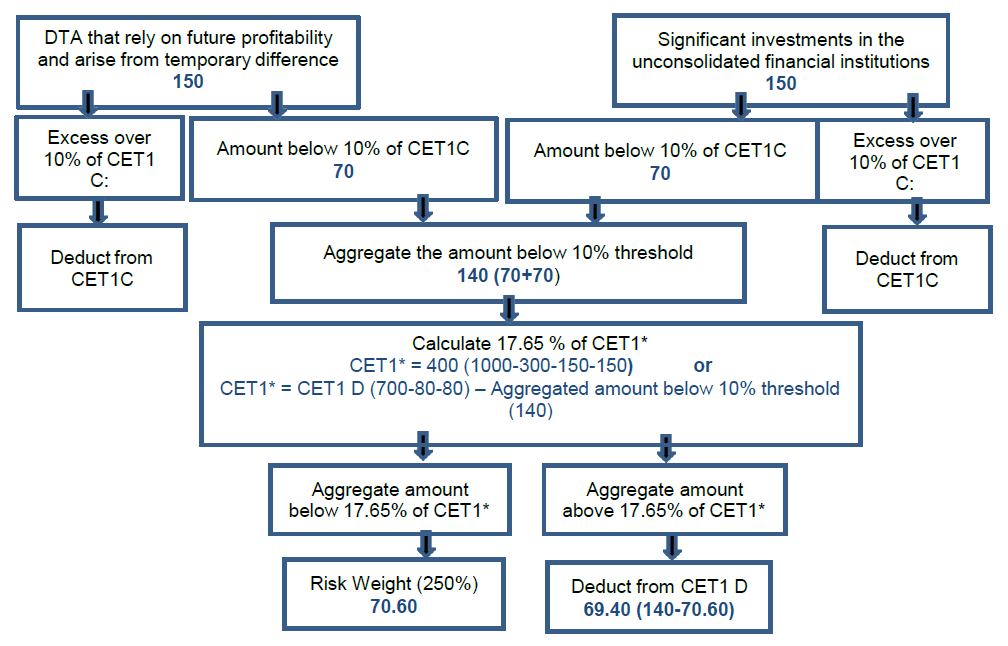

27. DTAs arising from net losses carried forward have to be deducted in full from a bank's CET1 (5.1.8.2). This recognises that their value can only be derived through the existence of future taxable income. On the other hand, a DTA relying on future profitability and arising from temporary timing differences is subject to the 'threshold deduction rule' (5.1.9.2).

- suffers a net loss in a financial year and is permitted to carry forward this loss to offset future profits when calculating its tax bill (net losses carried forward)

4. Threshold Deduction

28.The purpose of calculating the threshold is to limit the significant investments in the common shares of unconsolidated financial institutions (banks, insurance and other financial entities) and deferred tax assets (arising from temporary differences) to 15% of the CET1 after all deduction (Deduction includes regulatory deductions and the amount of significant investments in the common shares of unconsolidated financial institutions and deferred tax assets in full).

29.Therefore, significant investments in the common shares of unconsolidated financial institutions and deferred tax assets may receive limited recognition of 10% CET1 individually (CET after regulatory adjustment outlined in section 3 of the Tier Capital Supply Standard).

30.The amount that is recognised will receive risk weight of 250% and the remaining amount will be deducted.

See Appendix 5 for an example.

5. Significant Investment in Commercial Entities

31. For purposes of this section, 'significant investments' in a commercial entity is defined as any investment in the capital instruments of a commercial entity by a bank which is equivalent to or more than 10% of CET 1 of the bank (after application of regulatory and threshold deduction). See Appendix 3 for an example.

6. Frequently Asked Questions

Question 1: When will the Standards, Guidance and Template with regards to Solo reporting be issued by the Central Bank?

The Central Bank will issue all related material regarding Solo reporting during 2020. Formal communication will be issued in advance.Question 2: What is meant by the book value of an investment?

The book value of an investment shall be in accordance with the applicable accounting framework (IFRS). This valuation must be accepted by an external auditor.Question 3: Are capital shortfalls of non-consolidated insurance companies to be deducted from CET1?

Yes, any capital shortfall on a company has to be deducted.Question 4: If the Bank meets minimum CET1 ratios can the excess CET1 also be counted to meet AT1 and Total CAR?

Yes.Question 5: Please clarify whether minority interest related to any other regulated financial entity (which is not a bank) should be included or not.

Only minority interest of the subsidiary that are subject to the same minimum prudential standards and level of supervision as a bank be eligible for inclusion in the capital.Question 6: Is the bank able to include the profit & loss in the year-end CAR calculation before the issuance of the audited financial statements?

Bank may include interim profit/ yearend profit in CET1 capital only if reviewed or audited by external auditors. Furthermore, the expected dividend should be deducted in Q4.Question 7: Is subordinated Debt currently considered Tier 2 as per Basel III, hence no amortization is required?

Grandfathering rule plus amortization in last 5 years - refer to Standards for Capital Adequacy of banks in UAE, Tier Capital Supply Standard- paragraph 27 (iv)(b) . Reference should also be made to the Tier Capital Instruments Standards.Question 8: Do dividends need to be deducted from CET1 after the proposal from the Board or after Central Bank approval or after approval from shareholders at the Annual General Meeting?

Please refer to Question 6Question 9: How do you treat goodwill and intangible assets arising on an insurance subsidiary? Should it be considered since the standards mentions insurance subsidiaries are to be completely deconsolidated and hence there will be no goodwill?

Goodwill and other intangible must be deducted in the calculation of CET1. In particular deduction is also applied to any goodwill included in the valuation of significant investments in the capital of banking, financial and insurance entities that are outside the scope of consolidation.Question 10: Subsidiaries which are used for providing manpower services at cost, should these be classified as commercial entities or financial entities?

A non-financial sector entity is an entity that is not:- a)a financial sector entity; or

- b)a direct extension of banking; or

- c)ancillary to banking; or

- d)leasing, factoring, the management of unit trusts, the management of data processing services or any other similar services"

Question 11: Obtain an understanding to the timeline by when the Central Bank may advise specific Banks of specific countercyclical buffers?*

The underlying process for the implementation of countercyclical buffers will be set and communicated during 2018Question 12: Criterion 4 for Additional Tier 1 capital. Can the Central Bank give additional guidance on what will be considered to be an incentive to redeem?

The following list provides some examples of what would be considered to be an incentive to redeem:A call option combined with an increase in the credit spread of the instrument if the call is not exercised.

A call option combined with a requirement or an investor option to convert the instrument into shares if the call is not exercised.

A call option combined with a change in reference rate where the credit spread over the second reference rate is greater than the initial payment rate less the swap rate (ie the fixed rate paid to the call date to receive the second reference rate). For example, if the initial reference rate is 0.9%, the credit spread over the initial reference rate is 2% (ie the initial payment rate is 2.9%), and the swap rate to the call date is 1.2%, a credit spread over the second reference rate greater than 1.7% (2.9-1.2%) would be considered an incentive to redeem.

Conversion from a fixed rate to a floating rate (or vice versa) in combination with a call option without any increase in credit spread will not in itself be viewed as an incentive to redeem. However, as required by criteria 5, the bank must not do anything that creates an expectation that the call will be exercised.

The above is not an exhaustive list of what is considered an incentive to redeem and so banks should seek guidance from Central Bank on specific features and instruments. Banks must not expect Central Bank to approve the exercise of a call option for the purpose of satisfying investor expectations that a call will be exercised.

Question 13: Criteria 4 and 5 for Additional Tier 1 capital. An instrument is structured with a first call date after 5 years but thereafter is callable quarterly at every interest payment due date (subject to supervisory approval). The instrument does not have a step-up. Does instrument meet criteria 4 and 5 in terms of being perpetual with no incentive to redeem?

Criterion 5 allows an instrument to be called by an issuer after a minimum period of 5 years. It does not preclude calling at times after that date or preclude multiple dates on which a call may be exercised. However, the specification of multiple dates upon which a call might be exercised must not be used to create an expectation that the instrument will be redeemed at the first call date, as this is prohibited by criterion.Question 14: Can an option to call the instrument after five years but prior to the start of the amortisation period viewed as an incentive to redeem?

No, it can’t be viewed as an incentive to redeem.Question 15: With regards to countercyclical buffer, what are “private sector credit exposures”? What does “geographic location” mean? How should the geographic location of exposures on the banking book and the trading book be identified? What is the difference between (the jurisdiction of) “ultimate risk” and (the jurisdiction of) “immediate counterparty” exposures?*

“Private sector credit exposures” refers to exposures to private sector counterparties which attract a credit risk capital charge in the banking book, and the risk weighted equivalent trading book capital charges for specific risk, the incremental risk charge, and securitisation. Interbank exposures and exposures to the public sector are excluded, but non-bank financial sector exposures are included. The geographic location of a bank’s private sector credit exposures is determined by the location of the counterparties that make up the capital charge, irrespective of the bank’s own physical location or its country of incorporation. The location is identified according to the concept of “ultimate risk”. The geographic location identifies the jurisdiction that has announced countercyclical capital buffer add-on rate is to be applied by the bank to the corresponding credit exposure, appropriately weightedThe concepts of “ultimate risk” and “immediate risk” are those used by the BIS' International Banking Statistics. The jurisdiction of “immediate counterparty” refers to the jurisdiction of residence of immediate counterparties, while the jurisdiction of “ultimate risk” is where the final risk lies. For the purpose of the countercyclical capital buffer, banks should use, where possible, exposures on an “ultimate risk” basis.

For example, a bank could face the situation where the exposures to a borrower is in one jurisdiction (country A), and the risk mitigant (e.g. guarantee) is in another jurisdiction (country B). In this case, the “immediate counterparty” is in country A, but the “ultimate risk” is in country B. This means that if the bank has a debt claim on an investment vehicle, the ultimate risk exposure should be allocated to the jurisdiction where the vehicle (or if applicable, its parent/guarantor) resides. If the bank has an equity claim, the ultimate risk exposure should be allocated proportionately to the jurisdictions where the ultimate risk exposures of the vehicle resides.

*See current Countercyclical Capital Buffer on Credit Exposures in the UAE.

Appendix

Appendix 1: Banking, Securities, Insurance and Other Financial Entities - Significant Investment (Ownership in the Entity More Than 10%)

Significant investment (ownership in the entity more than 10% ) Entity Entity activity Investment Classification Listed/Unlisted Bank's ownership in the entity (% of Holding) Investment Amount A Banking Banking Book Listed 40% 60 B Insurance Banking Book Listed 18% 35 C Securities Banking Book Unlisted 16% 28 D Banking Trading Book Listed 11% 18 a. Total significant investment (Banking, Securities, insurance and other financial entities) 141 b. Bank's CET1 (after applying all the regulatory deduction except section 3.9 and 3.10 of the Tier Capital Supply Standard) 1000 c. Limit (10 % of bank's CET1) 100 d. Amount to be deducted from bank's CET1 41 e. Amount not deducted to considered for aggregate threshold deduction 100 The remaining amount of 100 is to be distributed amongst the investments on a pro rata / proportionate basis and risk weighted at 250% (assuming no threshold deduction apply).The total of 250 RWA (100 *250%) will be distributed as follows.

Entity Investment Classification Investment Amount as a % of all such investment Calculation of amount not deducted to be risk weighted Risk weight RWA Section A Banking Book 60 42% 43 (100 x 43%) 250% 106.38 Credit Risk B Banking Book 35 25% 25 (100 x 25%) 250% 62.06 Credit Risk C Banking Book 28 20% 20 (100 x 20%) 250% 49.65 Credit Risk D Trading Book 18 13% 13 (100 x 13%) Equity Risk - Market risk section 141 100% 100 Appendix 2: Banking, Securities, Insurance and Other Financial Entities - Investment with Ownership Not More Than 10%

Investment (ownership not more than 10%) Entity Entity activity Investment Classification Listed/Unlisted Bank's ownership in the entity (% of Holding) Investment Amount E Banking Banking Book Listed 10% 50 F Banking Trading Book Listed 3% 11 G Securities Banking Book Unlisted 8% 40 H Insurance Banking Book Listed 2% 9 a.Total investment (Banking, Securities, insurance and other financial entities) 110 b. Bank's CET1 (after applying all the regulatory deduction except section 3.9 and 3.10 of the Tier Capital Supply Standards) 1000 c. Limit (10% of bank's CET1) 100 d. Amount to be deducted from bank's CET1 (a-c) 10 e. Amount not deducted to be risk weighted (Remaining amount) (a-d) 100 The remaining amount of 75 is to be distributed amongst the investments on a pro rata / proportionate basis and risk weighted as stated below

Entity Investment Classification Investment Amount as a % of all such investment Calculation of amount not deducted to be risk weighted Listed/ Unlisted Risk weight RWA Section E Banking Book 50 45.5% 45.50 (100 x 45.5 %) Listed 100% 34.50 Credit Risk F Trading Book 11 10.0% 10 (100 x 10.00%) Listed Equity Risk - Market risk section G Banking Book 40 36.4% 36.4 (100 x 36.4%) Unlisted 150% 40.50 Credit Risk H Banking Book 9 8.2% 8.2 (100 x 8.2%) Listed 100% 6.00 Credit Risk 110 100% 100 Appendix 3: Significant Investments in Commercial Entities.

Individual Investment Limit Check and its treatment Bank's CET1 (after applying all the regulatory and threshold deduction) 1000 Individual Limit (10% of bank's CET1D) 100 Step 1: Individual Limit check

Significant investments in commercial entities Entity Entity activity Investment Classification Listed/ Unlisted Investment Amount Amount as a % of bank's CET1 Significant Investment Amount to RW at 952% Remaining amount I Commercial Banking Book Listed 140 14% Yes 40 100 J Commercial Banking Book Listed 120 12% Yes 20 100 K Commercial Banking Book Unlisted 110 11% Yes 10 100 L Commercial Banking Book Listed 115 12% Yes 15 100 M Commercial Banking Book Listed 75 8% No 75 N Commercial Banking Book Listed 45 5% No 45 O Commercial Banking Book Listed 50 5% No 50 655 85 570 Risk weighting at 952% on account of 10% threshold on individual basis is 85.

Step 2: Aggregate Limit check

Aggregate of remaining amount of investments after 10% deduction (entity I,J,K,L,M,N & O) 570 Aggregate Limit (25% of bank's CET1) 250 The amount to be risk-weighted at 952% based on the 25% threshold on aggregate basis 250 Remaining amount of investments to be risk-weighted under the applicable risk weighting rules (100% RW for listed and 150% unlisted) 320 Total amount to be risk weighted at 952%: 335 (85 + 250)

Appendix 4: Minority Interest Illustrative Example

This Appendix illustrates the treatment of minority interest and other capital issued out of subsidiaries to third parties, which is set out in section 2.7 of the Tier Capital Supply Standard (Paragraph 35 to 41).

A banking group consists of two legal entities that are both banks. Bank P is the parent, Bank S is the subsidiary, and their unconsolidated balance sheets are set out below

Bank P Balance sheet Amount (AED) Bank S Balance sheet Amount (AED) Assets Assets Loan to customers 100 Loan to customers 150 Investment in CET 1 of Bank S 7 Investment in AT1 of Bank S 4 Investment in T2 of Bank S 2 Total Assets 113 Total Assets 150 Liabilities and Equities Liabilities and Equities Depositors 70 Depositors 127 Common Equity (CET1) 26 Common Equity (CET1) 10 Additional Tier1 (AT1) 7 Additional Tier1 (AT1) 5 Tier 2 10 Tier 2 8 Total Liabilities and Equities 113 Total Liabilities and Equities 150 The balance sheet of Bank P shows that in addition to its loans to customers, it owns 70% of the common shares of Bank S, 80% of the Additional Tier 1 of Bank S and 25% of the Tier 2 capital of Bank S. The ownership of the capital of Bank S is therefore as follows:

Capital issued by Bank S Amount Issued to Parent Amount Issued to third party Total Common Equity (CET1) 7 3 10 Additional Tier1 (AT1) 4 1 5 Tier 1 11 4 15 Tier 2 2 6 8 Total Capital (TC) 13 10 23 The consolidated balance sheet of the banking group is set out below:

Consolidated Balance sheet of Bank P Assets Amount (AED) Loan to customers 250 Total Assets 250 Liabilities and Equities Depositors 197 Common Equity (CET1) 26 Additional Tier1 (AT1) 7 Tier 2 10 Minority Interest Common Equity (CET1) 3 Additional Tier1 (AT1) 1 Tier 2 6 Liabilities and Equities 250 For illustrative purposes, Bank S is assumed to have risk-weighted assets of 100. In this example, the minimum capital requirements of Bank S and the subsidiary’s contribution to the consolidated requirements are the same since Bank S does not have any loans to Bank P. This means that it is subject to the following minimum plus capital conservation buffer requirements and has the following surplus capital:

Minimum and surplus capital of Bank S Capital Minimum plus Capital conservation Buffer Surplus CET1 (7% + 2.5%) of 100 = 9.5 0.50

(10- 9.5)T1 (8.5%+ 2.5%) of 100 = 11 4.00

(10+5-11)TC (10.5% +2.5%) of 100 = 13 10

(10+5+8 -13)The following table illustrates how to calculate the amount of capital issued by Bank S to include in consolidated capital, following the calculation procedure set out in paragraphs 35 to 41 of the Tier Capital Supply Standards.

Bank S: amount of capital issued to third parties included in the consolidated capital. Capital Total Amount Issued (A) Total Amount Issued to third party (B) Surplus (C) Surplus attributable to third parties (i.e. amount excluded from consolidated capital) (D) = (C) * (B/A) Amount Included in the consolidated capital (E) = (B)-(D) CET1 10 3 0.5 0.15 2.85 T1 15 4 4 1.07 2.93 TC 23 10 10 4.35 5.65 The following table summarizes the components of capital for the consolidated group based on the amounts calculated in the table above. Additional Tier 1 is calculated as the difference between Common Equity Tier 1 and Tier 1 and Tier 2 is the difference between Total Capital and Tier 1.

Bank S: amount of capital issued to third parties included in the consolidated capital. Capital Total amount issued by Parent (all of which is to be included in consolidated capital) Amount issued by subsidiaries to third parties to be included in the consolidated capital Total amount of capital issued by parent and subsidiary to be included in the consolidated capital CET1 26 2.85 28.85 AT1 7 0.08 7.08 T1 33 2.93 35.93 T2 10 2.72 12.72 TC 43 5.65 48.65 Appendix 5: Threshold Deduction

This Appendix is meant to clarify the reporting of threshold deduction and calculation of the 10% limit on significant investments in the common shares of unconsolidated financial institutions (banks, insurance and other financial entities); and the 10% limit on deferred tax assets arising from temporary differences.

CET1 Capital (prior to regulatory deductions) 1000 Regulatory deductions: 300 Total CET1 after the regulatory adjustments above (CET1C) 700 Total amount of significant investments in the common share of banking, financial and insurance entities 150 Total amount of Deferred tax assets arising from temporary differences 150

*This is a “hypothetical” amount of CET1 that is used only for the purpose of determining the deduction of above two items for the aggregate limit. Amount of CET1 = Total CET1 (prior to deduction) – All the deduction except the threshold deduction (i.e. all deduction outlined in para 44 to 68 of the Tier Capital Supply Standards) minus the total amount of both DTA that rely on future profitability and arise from temporary difference and significant investments in the unconsolidated financial institutions.

Appendix 6: Effective Countercyclical Buffer

Assume a bank has the following capital ratios

Capital Base Minimum Capital Requirements Bank's Capital Ratio Common Equity Tier 1 Capital Ratio 7.00% 9.50% Tier 1 Capital Ratio 8.50% 0.00% Tier 2 Capital Ratio 2.00% 4.00% Total Capital Ratio 10.50% 13.50% From the above table, the bank has fulfilled all minimum capital requirements. In addition, the bank has to meet the additional capital buffers:

Capital Conservation Buffer (CCB) 2.50% Countercyclical Buffer* 0.00% D- SIB 1.00% Aggregated Buffer requirement (effective CCB) 3.50% The table below shows the adjusted quartiles accordingly:

Freely available

CET 1 RatioMinimum Capital Conservation Ratios (expressed as a percentage of earnings) Within 1st quartile of buffer: 0.0 % - 0.875% 100 % Within 2nd quartile of buffer: > 0.875% - 1.75% 80 % Within 3rd quartile of buffer: > 1.75% - 2.625% 60 % Within 4th quartile of buffer: > 2.625% - 3.5% 40 % Above top of the buffer: > 3.5% 0 % As the bank does not have Additional Tier 1, the bank has to use 8.5% of its available CET1 to fulfill the minimum Tier 1 requirement of 8.5%. Only the proportion of CET1 that is not allocated to fulfill the minimum capital requirements is freely available to fulfill the buffer requirement. For this bank, 1% CET1 is freely available, because the bank already used 8.5% of its CET1 to fulfill the Tier 1 ratio. (9.5% available CET1 - 8.5% CET1 required to fulfill the Tier 1 minimum requirement of 8.5%).

Impact: The bank breaches the effective CCB with 1% freely available CET1. Capital conservation is required by at least 80% of the bank’s earnings. Distributions to shareholders is limited to maximal 20% of the bank’s earnings (Central Bank approval of dividends still required).

*See current Countercyclical Capital Buffer on Credit Exposures in the UAE.

II. Tier Capital Instruments

Introduction

1.This guidance explains how banks should comply with the Tier Capital Instruments Standard. It must be read in conjunction with the Capital Regulation and Standards for Capital Adequacy of Banks in the UAE. It also ensures that banks issue robust and simple Tier capital instruments.

2.A bank needs to take into consideration the below points when issuing capital publicly or privately:

- a. The Central Bank expects that issuers will formulate the terms and conditions so that they are not complex, but as simple and as clear as possible.

- b. Prudential clauses of importance from a prudential point of view should not be written in italics. They should also not be worded in a way that makes it unclear whether they do actually apply (e.g. ‘it is expected that’, ‘if required by the regulation’, etc.). Terms and conditions must be worded clearly.

- c. The wording used must be in accordance with that in the Capital Standards/ Guidance.

- d. The text should avoid making references to ‘as determined by the bank’ or to regulatory reporting dates. All requirements must be fulfilled at any time.

- e. It is not desirable to specify the reference to say ‘under applicable law’ or ‘if required by the applicable banking rules’ when it is clear that legal requirements come directly from the Central Bank, Capital Regulation, Standards or as Guidance.

- f. A detailed list may easily create the impression that the list maybe exhaustive. The bank has to clearly note when a list is not exhaustive.

Distributable Items:

3.The definition of distributable items may change when the Central Bank introduces the solo level concept.

Subordination:

4.Additional Tier 1 instruments will rank below Tier 2 instruments by virtue of subordination. The instrument should not be subject to set-off or netting arrangements that would undermine the instrument's capacity to absorb losses.

Redemption Notices:

5.Where a notice has not been revoked as of the relevant date, it follows that a payment is due to the holder. Any non-payment thereafter may trigger an enforcement event. Any notice for redemption should become void and null as soon as the Central Bank declares that a PONV trigger event has occurred.

Call of Instruments:

- a. Optional Call:

The Central Bank does not prohibit the issuer to call the instrument at its option but only after a period of 5 years.

- b. Regulatory Call:

The Central Bank does not prohibit the issuer to call the instrument in case of a capital event so that they become or, as appropriate, remain, qualified regulatory capital. However, the amount in case of a capital event can be the outstanding amount or the amount that qualifies as regulatory capital, if some amount of the instrument is held by the issuer or whose purchase is funded by the issuer, save where such non-qualification is only as a result of any applicable limitation on the amount of such capital.

- c. Tax Call:

The Central Bank does not prohibit the issuer to call the instruments in case of a tax event. A tax event may occur at any time on or after the issue date. A tax event can occur as a result of a change in the applicable tax treatment of the instrument.

Note that both the optional call and the tax call require the Central Bank’s approval.

Changes of Terms and conditions:

a. Insignificant Changes to Terms and Conditions (Variation):

The issuer may vary the terms and conditions of the instrument subject to the condition of redemption in the Tier capital instrument Standard. Variation of the terms and conditions of the instrument can occur on optional call regulatory call, or tax call. Changes must be legally enforceable.

b. Significant Changes to Terms and Conditions:

Significant changes to the terms and conditions of the instrument will require the approval of the holders. Every instrument that undergoes significant changes needs to meet all requirements of the Tier Capital Instruments Standard.

Every instrument with changed terms and conditions need to be re-approved by the Central Bank by applying Stage 2 of the Approval Process in Appendix B of the Tier Capital Instruments Standard (Stage 1 of the Approval Process can be omitted in this case).

Coupon Payments:

6.No provision should link a change in payments to contractual, statutory or other obligations, as payments are fully discretionary. Payments should also not be linked to payments on other Additional Tier 1 instruments.

Dividend and Redemption Restrictions:

7.Dividend stopper arrangements that prevent for example dividend payments on common shares are not prohibited by the Central Bank. Furthermore, dividend stopper arrangements that prevent dividend payments on other Additional Tier 1 instruments are not prohibited by Central Bank. However, stoppers must not impede the full discretion that bank must have at all times to cancel distributions/payments on the instrument, nor must they act in a way that could hinder the recapitalization of the bank. For example, it would not be permitted for a stopper on an Additional Tier 1 instrument to:

- i. attempt to stop payment on another instrument where the payments on this other instrument were not also fully discretionary;

- ii. prevent distributions to shareholders for a period that extends beyond the point in time that dividends/coupons on the instrument are resumed;

- iii. impede the normal operation of the bank or any restructuring activity (including acquisitions/disposals).

8.A dividend stopper may act to prohibit actions that are equivalent to the payment of dividend, such as the bank undertaking discretionary share buybacks. The dividend stopper will remain until one coupon following the dividend stopper date has been made in full or an amount equal to the same has been duly set aside or provided for in full for the benefit of the holders of the instrument.

Maximum Distributable Amount (MDA):

To further clarify the MDA’s calculation, below is an example of the calculation:

Bank Capital Holdings 14.0% Bank Capital Requirements % CET1 7.0% AT1 1.5% Tier 2 2.0% Pillar 2 0.0% Capital Conservation Buffer 2.5% Countercyclical Buffer* 0.000% D-SIB Buffer 1.5% Total 14.5% Combined Buffer 4.0% Quartile of Buffer 1.0% Bank Capital Gap 0.5% Quartile 1 Quartile 2 Quartile 3 Quartile 4 0.0 1.0% 1.0% 2.0% 2.0% 3.0% 3.0% 4.0% The bank first will need to fulfill all minimum requirements. As the bank only has CET1 capital available, it needs to use CET1 capital to fulfill all minimum capital requirements (10.5%=7%+1.5%+2%). After fulfilling the minimum capital requirements, the bank has still 3.5% (=14.0%-10.5%) CET1 capital available to fulfill the combined buffer requirements of 4%. Hence, the Bank’s capital gap is 0.5%.

From the table above 3.5% means that the bank is in the fourth of the buffer requirements. Therefore, the MDA is restricted to 60% of the bank’s earnings, which means the bank may distribute no other restrictions and limitations considered, up to 60% of the earnings in the form of dividend, Additional Tier 1 payments, and variable remuneration.

Note that items considered to be distributions include dividends and share buybacks, discretionary payments on other Tier 1 capital instruments and discretionary bonus payments to staff. Payments that do not result in a depletion of CET1, which may for example include certain scrip dividends, are not considered distributions.

Note also that earnings are defined as distributable profits calculated prior to the deduction of elements subject to the restriction on distributions. Earnings are calculated after the tax, which would have been reported had none of the distributable items been paid. As such, any tax impact of making, such distributions are reversed out. Where a bank does not have positive earnings and has a CET1 ratio less than 9.5%, it would be restricted from making positive net distributions.

Gross-up Clauses:

Gross-up clauses for Additional Tier 1:

9.Gross up clauses are acceptable only if:

- i. It is activated by decision of the local tax authority of the issuer and not the investor,

- ii. The increased payments do not exceed distributable items,

- iii. The gross-up is in relation to the dividend and not the principal.

Gross up Clauses for Tier 2:

10.The second condition related to distributable items is not relevant for Tier 2 instruments, as Tier 2 coupons are not restricted by the amount of available distributable items. Therefore, Tier 2 gross-up clauses can be considered as acceptable if they are activated by a decision of the local tax authority of the issuer, and if they relate to dividend and not on principal. The other two conditions on gross-up clauses are, however, activation is still required by a local tax authority of the issuer and not the investor, and the gross-up is in relation to the dividend payments only not principal.

Point of Non-Viability (PONV):

11.The issuance of any new shares as a result of the Point of Non-Viability must occur prior to any public sector injection of capital so that the capital provided by the public sector is not diluted.

Further guidance on grandfathering:

12.If a Tier 2 instrument eligible for grandfathering begins its final five-year amortisation period prior to 1st January 2018, the base for grandfathering in this case must take into account the amortised amount, not the full nominal amount. As for the rate, if a Tier 2 instrument eligible for grandfathering begins its final amortisation period on 1st January 2018, then individual instruments will continue to be amortised at a rate of 20% per year while the grandfathering cap will be reduced at a rate of 10% per year. Note that each tranche needs to be treated as a separate tranche.

Amortisation of Tier 2 instruments:

13.During the last 5 years of the eligibility before maturity, the eligibility of Tier 2 instruments is written down by 20% per year, i.e. the eligible amount is calculated by multiplying:

- i. The nominal amount of the instruments on the first day of the final five year period of their contractual maturity divided by the number of calendar days in that period;

- ii. The number of remaining calendar days until the contractual maturity of the instruments.

Documents required to be submitted for the application to issue new Tier Capital Instruments

- 1.The CN-01 form should be completed, filled and signed by the bank's Chief Executive Officer (CEO), Chief Financial Officer (CFO), Head of Internal Audit, Head of Compliance and Head of Risk.

- 2.Full terms and conditions, together with the risk factors relating to the instrument.

- i. Instruments of Islamic banks issued through an SPV must also provide the contract between the bank and the SPV

- i. Instruments of Islamic banks issued through an SPV must also provide the contract between the bank and the SPV

- 3.Shareholder Approval:

- i. Tier capital instruments require shareholder approval.

- ii. The approval shall relate to an issuance of the specific planned Tier capital instrument (Additional Tier 1 or subordinated Tier 2). Moreover, the approval should clearly mention that the instrument is subordinated; coupon payments may not be paid under certain circumstances, and contains a Point of Non-Viability (PONV) condition.

- i. Tier capital instruments require shareholder approval.

- 4.Legal opinion letters:

- i. Legal Opinion of an independent appropriately qualified and experienced lawyer that the terms and conditions are compliant with the requirements detailed in the Capital Regulations, Standards and Guidance.

- ii. Legal opinion of an independent appropriately qualified and experienced lawyer that the obligations contained in terms and conditions will constitute legal, valid, binding and enforceable obligations.

- iii. Legal opinion of an independent appropriately qualified and experienced lawyer that the Self-Assessment of the issuing bank meets the Conditions and the Capital Regulations

- i. Legal Opinion of an independent appropriately qualified and experienced lawyer that the terms and conditions are compliant with the requirements detailed in the Capital Regulations, Standards and Guidance.

- 5.Capital planning and forecast:

The Business as Usual (BAU) case should be formulated, such as:

- a) Amount of assumed issuance and the expected issuance date (e.g. Q1 2018).

- b) Capital structure: % in CET1, AT1, Tier 2 and deductions (using Basel 3 capital components)

- c) Five (5) year forecast of the Balance sheet, Profit & loss P&L, Risk Weighted Assets RWA.

- d) Amortization of Tier Capital Issuances: Subordinated Tier 2 in the last 5 years prior to maturity and AT1 Instruments, if they fall under a grandfathering rule, for example, 10% per year.

- e) Key assumptions and analysis (e.g. on balance growth, asset structure, conversation factors CCF for off balance, operational and market risk, total assets growth, of which businesses that will be the main driver for such growth) and CRWA (i.e. on balance sheet exposure in different industry) in numerical as well as qualitative aspect.

6. Stress Testing Scenarios:

The Stress Testing should be submitted in form of a presentation including the underlying data in Excel sheet.

Two Scenarios should be provided as part of the presentation:

- a) Top 2 customers defaulting (point in time analysis permitted: End of Year): Definition of top 2 customers; name of top 2 customers; exposure (including on and off balance exposures); what type of eligible collateral and value of collateral, with two sub-scenarios:

- i. With average provisioning level of similar assets, and

- ii.75% provisioning level

- i. With average provisioning level of similar assets, and

- b) Central Bank’s Macro-Economic Stress Test

- •Assumptions and results of the latest Macroeconomic stress tests performed by the Central Bank.

- 7.Non-Funding Notice: Neither the bank nor a related party over which the bank exercises control or significant influence can have purchased the instrument, nor can the bank directly or indirectly have funded the purchase of the instrument.

- Private Placements

- •Offer letter is required for private placements, including risk factors and the bank's financial and risk situation.

- •Market Conformity Analysis: The bank has to provide evidence on why the pricing of the instrument conforms to the market rate.

*See current Countercyclical Capital Buffer on Credit Exposures in the UAE.

- a. The Central Bank expects that issuers will formulate the terms and conditions so that they are not complex, but as simple and as clear as possible.

Frequently Asked Questions (FAQ)

Question 1: The last bullet point mentions “Liability accounted instruments must set the loss absorption trigger at a level of 7.625%.” Is it Central Bank decision to have this trigger set at 7.625%? Are any triggers likely to be set for equity accounted instruments?

It is Central Bank’s decision for the trigger level. However, the trigger level derives directly from Basel. Minimum capital requirement plus 0.625%. Note, that the consultation documents do not consult on a trigger for equity accounted AT1. However, in particular in conjunction with the development of a recovery/ resolution regulation, the introduction of a trigger level may also be discussed again, as pointed out in the presentation that was circulated with the Tier capital instrument documents.

Question 2: Point of Non-Viability mentions that “A Point of Non-Viability means that the Regulator has determined that the issuer has or will become, Non-Viable without: (a) a Write-down; or (b) a public injection of capital (or equivalent support).”. We need clarification as to whether the PONV will be determined by the regulator or the issuer. Also, please advise under what circumstance will partial Write-down be permitted.

The regulator determines whether the bank is non-viable or not. Partial write-down will be permitted only for exceptional cases. Explicit examples will not be provided to prevent any expectation.

Question 3: Appendix A: Application Process 1.4: It is mentioned that “Stress Testing with a stress scenario of top 2 customers are defaulting”. Since many UAE banks have concentrations in this area, what loss rate needs to be applied in this stress scenario?

Current status quo is two sub scenarios: 75% loss rate and average loss rate of the bank for such customers.III. Credit Risk

I. Introduction

1. This section provides the guidance for the computation of Credit Risk Weighted Assets (CRWAs) under the Standardised Approach (SA). This guidance should be read in conjunction with the Central Bank’s Standard on Credit Risk.

2. A bank must apply risk weights to its on-balance-sheet and off-balance-sheet items using the risk- weighted assets approach. Risk weights are based on credit ratings or fixed risk weights and are broadly aligned with the likelihood of obligor or counterparty default.

3. A bank may use the ratings determined by an External Credit Assessment Institution (ECAI) for credit ratings. In general, banks should only use solicited ratings from recognised ECAIs for the purposes of calculating capital requirement under the SA. However, in exceptional cases, the bank may use unsolicited ratings with the Central Bank approval.

4. Note that all exposures subject to the SA should be risk weighted net of specific allowances and interest in suspense. The guidance must be read in conjunction with Securitisation, Equity Investments in Funds, Counterparty Credit Risk and Credit Valuation Guidance.

5. The guidance set out in this section applies to all exposures in the banking book. Exposures in the trading book should be captured as part of a bank’s market risk capital calculations.

II. Clarification and Guiding Principles

A. Claims on Sovereigns

6. UAE Sovereigns: The UAE Sovereign asset class consists of exposures to Federal Government and Emirates governments.

7. Federal Government includes all the UAE Federal entities and Central Bank of the UAE (Central Bank). Banks have transition period of 7 years from the date of implementation for exposures to Federal Government that receive a 0% RW, if such exposures are denominated in AED or USD and funded in AED or USD. However, any claim on UAE Federal Government in foreign currency other than USD should be risk weighted according to the published credit risk rating of UAE Federal Government. In the absence of solicited rating for UAE Federal Government, unsolicited ratings are permissible for assigning risk weights for UAE Federal Government exposures.

8. Emirates Governments’ exposures include exposures to the Ruler and the Crown Prince of each emirate acting in the capacity as ruler and crown prince, as well as exposures to the ministries, municipalities and other Emirates government departments. Banks have transition period of 7 years from the date of implementation for exposures to Emirates Governments that receive a 0% RW, if such exposures are denominated in AED or USD and funded in AED or USD. Any claim on Emirates governments in a foreign currency other than USD should be risk weighted according to the rating of the Emirate Government.

9. GCC Sovereigns: If the regulators in GCC exercise their discretion to permit banks in their jurisdiction to allocate a lower risk weight to claims on that jurisdiction’s sovereign, denominated in the domestic currency of that jurisdiction and funded in that currency, the same, lower risk weight may be allocated to such claims (e.g. 0% assigned to the Government of Saudi Arabia if the exposure is denominated and funded in SAR). This is limited only to GCC sovereign exposures and this lower risk weight may be extended to the risk weighting of collateral and guarantees (refer to section on credit risk mitigation).

10. All other exposures to sovereigns should be risk weighted according to the sovereign rating even if the national supervisory authority adopts preferential risk weights.

B. Claims on Public Sector Entities (PSEs)

Non-Commercial PSEs

11. Non-Commercial PSEs include administrative bodies responsible to the UAE Federal Government, to the Emirates Governments, or to local authorities and other non-commercial undertakings owned by the Federal governments, Emirates Governments or local authorities. These non-commercial PSEs do not have specific revenue- raising powers or specific institutional arrangements the effect of which is to reduce their risks of default. The risk of non-commercial PSE exposures is not equivalent to the risk of sovereign exposures and hence the treatment of claims on sovereigns cannot be applied to non-commercial PSE. However, in exceptional cases, a Non-Commercial PSE may receive the same treatment as its sovereign, if the entity has proven formal arrangements in place to the effect that there is no distinction between the risk of the entity and the risk of its sovereign. The Central Bank's GRE List would reflect this accordingly.

12. If the UAE borrower satisfies the criteria in paragraph 13, the risk weight shall be the same as that for claims on banks. However, the preferential treatment for short-term claims on banks may not be applied. In particular, unrated non-commercial PSE qualify for 50% risk weight. The criteria are based on the principle that non-commercial PSEs qualify for lower risk weights because they have significantly lower risk than a commercial company does. In addition, banks are specifically required to ensure compliance with other aspects of the banking regulations when lending to these entities, for example, but not limited to, the Central Bank large exposure regulations.

13. The alternative criteria listed are to be applied in determining whether an entity qualifies for treatment as a non-commercial PSE. The Central Bank provides a list (so-called GRE List) to all the banks in the UAE which includes non-commercial PSEs.

i. Direct government (Federal or Emirate) ownership >50% directly or through a qualifying PSE that itself is majority owned by government.

ii. An entity whose complete activities are functions of a government.

iii. Its services are of public benefit including when services are sold directly to the public (e.g. electricity and water). The service provided should be of substantial public benefit and the entity should have a monopolistic nature and there should be a significant likelihood that the government would not let the entity go bankrupt.

iv. Not listed on any stock exchange.

v. Provides internal services to parent or sister companies only, and the parent company is itself a non-commercial PSE.

vi. The function of the company is of a non-commercial nature and does not operate in a competitive market.

vii. Does not operate overseas. 14. In the case of a UAE sovereign guarantee given to a non-commercial PSE, with the Central Bank approval, the guarantee may be treated as eligible credit risk mitigation (CRM) to reduce the exposure provided the bank ensures compliance with the entire minimum regulatory requirements and operational requirements stated in the credit risk standard.

Government Related Entities (GRE)

15. These are commercial undertakings that are fully owned or more than 50% in ownership by Federal governments, or by Emirates governments. As these entities function as a corporate in the competitive markets even though the government is the major shareholder, Central Bank requires such exposures to be classified under GRE and get the same treatment of claims on corporate with the appropriate risk weights based on the credit rating of the entity.

16. All banks must comply with the latest version of the GRE list for classification and risk weighting of entities. Banks that have information that would lead to the addition (or removal) of an entity to (or from) the GRE list must submit such information to the Central Bank. All banks must comply with the GRE list unless any addition or removal of entities is reflected in the GRE list.

17. Banks Internal audit/compliance department should perform regular reviews to ensure the PSE and GRE classification complies with the Central Bank GRE list.

C. Claims on Multilateral Development Banks (MDBs)

18. Exposures to MDBs shall in general be treated similar to claim on banks, but without using the preferential treatment for short term claims. However, highly rated MDBs, which meet certain criteria specified below, are eligible for a preferential 0% risk weight.

i. Very high quality long-term issuer ratings, i.e. a majority of an MDB's external assessments must be AAA;

ii. Shareholder structure is comprised of a significant proportion of sovereigns with long-term issuer credit assessments of AA- or better, or the majority of the MDB's fund-raising is in the form of paid-in equity/capital and there is little or no leverage;

iii. Strong shareholder support demonstrated by the amount of paid-in capital contributed by the shareholders; the amount of further capital the MDBs have the right to call, if required, to repay their liabilities; and continued capital contributions and new pledges from sovereign shareholders;

iv. Adequate level of capital and liquidity (a case-by-case approach is necessary in order to assess whether each MDB's capital and liquidity are adequate), and

v. Strict statutory lending requirements and conservative financial policies, which would include among other conditions a structured approval process, internal creditworthiness and risk concentration limits (per country, sector, and individual exposure and credit category), large exposures approval by the board or a committee of the board, fixed repayment schedules, effective monitoring of use of proceeds, status review process, and rigorous assessment of risk and provisioning to loan loss reserve. 19. MDBs currently eligible for 0% risk weight are the World Bank Group comprised of the International Bank for Reconstruction and Development, the International Finance Corporation, the Multilateral Investment Guarantee Agency and the International Development Association, the Asian Development Bank, the African Development Bank, the European Bank for Reconstruction and Development, the Inter-American Development Bank, the European Investment Bank, the European Investment Fund, the Nordic Investment Bank, the Caribbean Development Bank, the Islamic Development Bank, the Council of Europe Development Bank, the International Finance Facility for Immunisation and the Asian Infrastructure Investment Bank. The list of MDBs is by the Basel Committee on Banking Supervision (BCBS) and can be found on the website www.bis.org. All banks are required to refer to and comply with the BCBS list. Whilst the BCBS evaluates the eligibility of the entities on a case-by-case basis, the Central Bank has no role in the assessment and decision of entities being eligible for 0% risk weight.

D. Claims on Banks

20. The types of claims that fall under this asset class are claims not limited to those due from banks, nostro accounts, certificates of deposit (CD) issued by banks, and repurchase agreements (repos). A risk weight of 50% (long term) and 20% (short term) is applied to claims on unrated banks. However, this treatment is subject to the provision that no claim on an unrated bank may receive a risk weight lower than that applied to claims on its sovereign of incorporation.

21. Exposure to intra-group of the bank have to be risk weighted according to the external rating of the counterparty entity (e.g. exposures to the head office shall receive the risk weight according to the rating of the head office).

E. Claims on Securities Firms

In addition to providing loans to other banks in the interbank market, banks provide loans to securities firms. The securities firms use these loans to fund the purchase of securities. Exposures to these securities firms shall be treated as claims on banks if these firms are subject to prudential standards and a level of supervision that is equivalent to those applicable to banks. Such supervision must include at least both capital and liquidity requirements. Exposures to all other securities firms that are not treated as claims on banks will be treated as exposures to corporates.

F. Claims on Corporates

22. For the purposes of calculating capital requirements, exposures to corporates include, but are not limited to, exposures (loans, bonds, receivables, etc.) to incorporated entities, associations, partnerships, proprietorships, trusts, funds and other entities with similar characteristics, except those which qualify for one of the other exposure classes. The corporate exposure class does not include exposures to individuals.

23. Claims on corporates may be risk- weighted based on the entity’s external credit rating assessment. The Central Bank may increase the standard risk weight for unrated claims where it judges that a higher risk weight is warranted by the overall default experience. As part of the supervisory review process, the Central Bank may also consider whether the credit quality of corporate claims held by banks warrants a risk weight higher than 100%.

G. Claims Included in the Regulatory Retail Portfolios

To qualify for a 75% risk weight in the regulatory retail portfolio, claims must meet the four criteria stated in the Credit Risk Standard (orientation criterion, product criterion, granularity criterion and value criterion). All other retail claims should be risk weighted at 100%. For granularity criterion and value criterion, the aggregated exposure means gross amount (i.e. not taking any credit risk mitigation into account) of all forms of retail exposures, excluding residential real estate exposures. In case of off-balance sheet items, the gross amount will be calculated after applying credit conversion factors. In addition, “to one counterparty” means one or several entities that may be considered as a single beneficiary (e.g. in the case of a small business that is affiliated to another small business, the limit would apply to the bank’s aggregated exposure on both businesses).

24.Claims secured by residential property and past due retail loans are to be excluded from the overall regulatory retail portfolio for risk weighting purposes. These are addressed separately in the asset classes for residential property or commercial real estate.

H. Claims Secured by Residential Property

25. Claims secured by residential property are defined as loans secured by residential property that is either self-occupied or rented out. The property must be fully mortgaged in favor of the bank.

26. The Loan-to-Value (LTV) ratio is the outstanding loan exposure divided by the value of the property. The value of the property will be maintained at the value at origination unless the Central Bank requires banks to revise the property value downward. The value must be adjusted if an extraordinary, idiosyncratic event occurs resulting in a permanent reduction of the property value. Such adjustment must be notified to the Central Bank. If the value has been adjusted downwards, a subsequent upwards adjustment can be made but not to a higher value than the value at origination.

27. A 35% risk weighting shall apply to eligible residential claims if the LTV ratio is less than 85% and the exposure is less than AED 10 million. When the loan amount exceeds AED 10 million and the LTV is below 85%, the loan amount up to AED 10 million will receive 35% risk weight and the remaining amount above AED 10 million receives 100% risk weight.

28. A risk weight of 75% may be applied by banks that do not hold information regarding LTVs for individual exposures

29. For residential exposures that meet the criteria for regulatory retail claims and have an LTV greater than 85%, the 75% risk weight must be applied to the whole loan, i.e. the loan should not be split.

30. The risk-weights in this asset class may be applied to a limit of four individual properties made to a single individual customer that are owner- occupied or rented out by a retail borrower. Any additional exposure to a customer with loans for four individual properties shall be classified as a claim on a commercial property and risk weighted with 100%.

I. Claims Secured by Commercial Real Estate

31. Commercial real estate is defined as a loan granted by a bank to a customer specifically for the purpose of buying or constructing commercial property including residential towers and mixed use towers.

J. Past Due Loans

32. Risk weights of past due loans depend on the degree of provision coverage on the claim. For any past due loan, 100% Credit Conversion Factor (CCF) should be applied for the off-balance sheet component to calculate the credit risk-weighted assets. Any exposure that is past due for more than 90 days should be reported under this asset class, net of specific provisions (including partial write-offs). This differs from the IFRS 9 classification as the past due asset includes any loans more than 90 days past due.

K. Higher-Risk Categories

33. Higher risk weights may be applied to assets that reflect higher risks. A bank may decide to apply a risk weight of 150% or higher.

L. Other Assets

34.Assets in this class include any other form of exposure that does not fit into the specific exposure classes. The standard risk weight for all other assets will be 100%, with the exception of the following exposures:

a) 0% risk weight applied to

i. cash owned and held at the bank or in transit;

ii. Gold bullion held at the bank or held in another bank on an allocated basis, to the extent the gold bullion assets are backed by gold bullion liabilities;

iii. All the deductions from capital according to the Tier capital supply of Standards of Capital Adequacy in the UAE, for reconciliation between the regulatory return and the audited/reviewed financial statement.

b) 20% risk weight:

i. Cash items in the process of collection.

c) 100% risk weight

i. Investments in the capital of banking, financial and insurance entities to which a credit risk standardised approach applies, unless they are deducted from regulatory capital according to section 3.9 of Tier capital supply of Standards Capital Adequacy in the UAE. (listed entity)

ii. Investments in commercial entities below the materiality thresholds according to section 5 of Tier capital supply of Standards of Capital Adequacy in the UAE (listed);

iii. Premises, plant and equipment and other fixed assets,

iv. Prepaid expenses such as property taxes and utilities,

v. All other assets

d) 150% risk weight

i. The amount of investments in the capital of banking, financial and insurance entities to which a credit risk standardised approach applies unless they are deducted from regulatory capital deduction according to section 3.9 of Tier capital supply of Standards of Capital Adequacy in the UAE (unlisted entity);

ii. Investments in commercial entities below the materiality thresholds according to section 5 of Tier capital supply of Standards of Capital Adequacy in the UAE (unlisted entity).

e) 250% risk weight

i. Investments in the capital of banking, financial and insurance entities to which a credit risk standardised approach, applies unless they are deducted from regulatory capital according to the threshold deduction described in section 3.10 of Tier capital supply of Standards of Capital Adequacy in the UAE.

ii. Deferred tax assets (DTAs) which depend on future profitability and arise from temporary differences unless they are not deducted under threshold deductions described in section 4 of Tier capital supply of Standards of Capital Adequacy in the UAE.

f) 1250% risk weight

i. Investments in commercial entities in excess of the materiality thresholds must be risk-weighted at 1/ (Minimum capital requirement) (i.e. 1250%).

M. Off-Balance Sheet Items: Credit Conversion Factors

35.Under the standardised approach, off-balance sheet items are converted into credit exposure equivalents with Credit Conversion Factors (CCFs). CCFs approximate the potential amount of the off-balance sheet facility that would have been drawn down by the client by the time of its default. The credit equivalent amount is treated in a manner similar to an on-balance sheet instrument and is assigned the risk weight appropriate to the counterparty. The categories of off-balance sheet and its appropriate CCFs are outlined in the standard.

Calculating credit equivalent amounts for off-balance sheet item:

(Principal amount – provision amount) * CCF = Credit equivalent amount.

Bank guarantees

36.There are two types of bank guarantees viz. financial guarantees (direct credit substitutes); and performance guarantees (transaction-related contingent items).

37.Financial guarantees essentially carry the same credit risk as a direct extension of credit i.e. the risk of loss is directly linked to the creditworthiness of the counterparty against whom a potential claim is acquired, and therefore attracts a CCF of 100%.

38.Performance guarantees are essentially transaction-related contingencies that involve an irrevocable undertaking to pay a third party in the event the counterparty fails to fulfil or perform a contractual non-financial obligation. In such transactions, the risk of loss depends on the event which need not necessarily be related to the creditworthiness of the counterparty involved. Performance guarantees attract a CCF of 50%.

Commitments

39.The credit conversion factor applied to a commitment is dependent on its maturity. Banks should use original maturity to report these instruments.

40.Longer maturity commitments are considered to be of higher risk because there is a longer period between credit reviews and less opportunity to withdraw the commitment if the credit quality of the customer deteriorates. Commitments with an original maturity up to one year and commitments with an original maturity over one year will receive a CCF of 20% and 50%, respectively.

41.However, any commitments that are unconditionally cancellable at any time by the bank without prior notice, or that effectively provide for automatic cancellation due to deterioration in a borrower’s creditworthiness, will receive a 0% CCF. This requires that banks conduct formal reviews of the facilities regularly and this provides the opportunity to take note of any perceived deterioration in credit quality and thereby cancellability by the bank.

42.For exposures that give rise to counterparty credit risk, the exposure amount to be used in the determination of RWA is to be calculated according to the standardised approach for Counterparty Credit Risk (SA-CCR).

N. Credit Risk Mitigation (CRM)

43.Only eligible collateral, guarantees, credit derivatives, and netting under legally enforceable bilateral agreements (such as ISDAs) are eligible for CRM purposes. For example, a commitment to provide collateral or a guarantee is not recognised as an eligible CRM technique for capital adequacy purposes until the commitment to do so is actually fulfilled.

44.No additional CRM will be recognised for capital adequacy purposes on exposures where the risk weight is mapped from a rating specific to a debt security where that rating already reflects CRM. For example, if the rating has already taken into account a guarantee pledged by the parent or sovereign entity, then the guarantee shall not be considered again for credit risk mitigation purposes.

45.Banks should ensure that all minimum legal and the operational requirements set out in the Standard are fulfilled.

CRM treatment by substitution of risk weights

46.The method of substitution of risk weight is applicable for the recognition of the guarantees and credit derivatives as CRM techniques under both the simple approach and the comprehensive approach. Under this method, an exposure is divided into two portions: the portion covered by credit protection and the remaining uncovered portion.

47.For guarantees and credit derivatives, the value of credit protection to be recorded is the nominal value. However, where the credit protection is denominated in a currency different from that of the underlying obligation, the covered portion should be reduced by a standard supervisory haircut defined in the Credit Risk Standard for the currency mismatch.

48.For eligible collateral, the value of credit protection to be recorded is its market value, subject to a minimum revaluation frequency of 6 months for performing assets, and 3 months for past due assets (if this is not achieved then no value can be recognised). Where the collateral includes cash deposits, certificates of deposit, cash funded credit-linked notes, or other comparable instruments, which are held at a third-party bank in a non-custodial arrangement and unconditionally and irrevocably pledged or assigned to the bank, the collateral will be allocated the same risk weight as that of the third-party bank.

Simple Approach

49.Under simple approach, the eligible collateral must be pledged for at least the life of the exposure, i.e. maturity mismatch is not allowed.

50.Where a bank has collateral in the form of shares and uses the simple approach, a 100% risk weight is applied for listed shares and 150% risk weight for unlisted shares.

Comprehensive Approach

51.Under the comprehensive approach, the collateral adjusted value is deducted from the risk exposure (before assigning the risk weight). Standard supervisory haircuts as defined in the Credit Risk Standard are applied to the collateral because collateral is subject to risk, which could reduce the realisation value of the collateral when liquidated.

52.If the exposure and collateral are held in different currencies, the bank must adjust downwards the volatility- adjusted collateral amount to take into account possible future fluctuations in exchange rates.

53.There is no distinction for applying supervisory haircuts between main index equities and equities listed at a recognised exchange. A 25% haircut applies to all equities.

Capital Add-on under Pillar 2

54.While the use of CRM techniques reduces or transfers credit risk, it gives rise to other risks that need to be adequately controlled and managed. Banks should take all appropriate steps to ensure the effectiveness of the CRM and to address related risks. Where these risks are not adequately controlled, the Central Bank may impose additional capital charges or take other supervisory actions as outlined in Pillar 2 Standard.

III. Shari’ah Implementation

55. Banks that conduct all or part of their activities in accordance with the provisions of Shari’ah laws and have exposure to risks similar to those mentioned in the Credit Risk Standard, shall, for the purpose of maintaining an appropriate level of capital, calculate the relevant risk weighted asset in line with these guidelines. This must be done in a manner compliant with the Shari’ah laws.

56. This is applicable until relevant standards and/or guidelines in respect of these transactions are issued specifically for banks offering Islamic financial services.

IV. Frequently Asked Questions (FAQ)

During the industry consultation the Central Bank received a number of questions related to the Credit Risk Standard and Guidance. To ensure consistent implementation of the Credit Risk Standard in the UAE, the main questions are addressed hereunder.

Claims on Sovereigns

Question 1: What does the 7-year transition for USD exposure to the Federal Government and Emirates Government mean for banks?

During the 7-year transition period, banks are required to have a forward looking plan on USD exposures to Federal and Emirate governments. Banks shall monitor and manage the impact of the change in risk weights of exposures in USD on the bank’s capital position. Exposures in USD as well as the banks’ capital plans will be monitored by the Central Bank.Question 2: What is the appropriate risk weight for exposures to other GCC sovereigns?

A 0% risk weight is applied to GCC Sovereign exposures denominated and funded in the domestic currency of their country. However, exposures in non-domestic currencies (including USD) shall be risk weighted according to the rating of sovereigns.Question 3: Does the Central Bank allow banks to apply unsolicited ratings in the same way as solicited ratings?

Bank should use ratings determined by an eligible External Credit Assessment Institution (ECAIs). Only solicited ratings are allowed to be used. The Central Bank only allows unsolicited ratings from an eligible ECAI for the UAE federal government. All other exposures shall be risk weighted using solicited ratings.Claims on Non-Commercial Public Sector Enterprises

Question 4: Can the bank include claims on a GCC PSE denominated in their local currency under claims of Non-Commercial PSEs?

No, the preferential risk weights for Non-Commercial PSEs are only granted for UAE entities.Question 5: Do all the seven criteria stated in the credit risk guidance have to be met or any of the criterion can be met to classify an entity as non-commercial PSE? In addition, does the bank just follow the so-called GRE list or shall the bank apply the criteria to classify entities as non-commercial PSE?

To classify entities as Non-commercial PSE, the Central Bank will consider in its approval process all seven criteria and in principle all seven criteria must be satisfied. A bank may approach the Central Bank, if the bank thinks that certain entities satisfy the criteria for a Non-commercial PSE that can be added to the GRE list. If banks have information that would lead to changes to of the GRE List, banks should inform the Central Bank accordingly.Question 6: The guidance requires that the bank’s internal audit/ compliance departments perform regular reviews to ensure the PSE and GRE classification complies with the Central Bank's GRE list. What is the expected frequency of such a review?

The frequency of internal audit/compliance should be commensurate with the bank's size, the nature and risks of bank’s operations and the complexity of the bank.Claims on Multilateral Development Banks (MDBs)

Question 7: Does an MDB need to satisfy all of the stated criteria or any one of the criteria to apply a 0% risk-weight?

Exposures to MDBs may receive a risk weight of 0% if they fulfill all five criteria. However, the Central Bank does not decide whether an MDB satisfies the criteria or not. The Basel Committee on Banking Supervision (BCBS) evaluates each MDB’s eligibility for inclusion in the list of 0% RW on a case-by-case basis.Claims on Banks

Question 8: For claims on an unrated bank, can the bank apply the preferential rating as per risk weight table for short-term exposures?

A risk weight of 50% for long term exposures and 20% for short term exposures are applied to claims on unrated banks. However, no claim on an unrated bank may receive a risk weight lower than the risk weight applied to claims on its sovereign of incorporation, irrespectively of the exposure being short-term or long-term.Claims on Corporates

Question 9: Should loans to High Net Worth Individuals (HNIs) be reported under claims in regulatory retail portfolio or claims on corporate?