III. Example Calculations

A. Standardised Approach

33.Consider a bank applying the SEC-SA to a securitisation exposure for which the underlying pool of assets has a required capital ratio of 9% under the standardised approach to credit risk. Suppose that the delinquency rate is unknown for 1% of the exposures in the underlying pool, but for the remaining 99% of the pool the delinquency rate is known to be 6%. The bank holds an investment of 100 million in a tranche that has an attachment point of 5% and a detachment point of 25%. Finally, assume that the pool does not itself contain any securitisation exposures, so the exposure is not a resecuritisation.

34.In this example, KSA is given at 9%. To adjust for the known delinquency rate on the pooled assets, the bank computes an adjusted capital ratio:

(1 − W) × KSA + (W × 0.5) = 0.94 × 0.09 + 0.06 × 0.5 = 0.1146

35.This calculated capital ratio must be further adjusted for the fact that the delinquency rate is unknown for a small portion (1%) of the underlying asset pool:

KA = 0.99 × 0.1146 + 0.01 = 0.1235

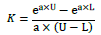

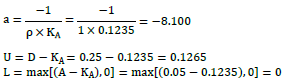

36.Next, the bank applies the supervisory formula to calculate the capital required per unit of securitisation exposure, using the values of the attachment point A, the detachment point D, the calculated value of KA, and the appropriate value of the supervisory parameter ρ, and noting that D>KA:

where:

Note that because this is not a resecuritisation exposure, the appropriate value of the supervisory calibration parameter rho is 1 (ρ=1).

37.Substituting the values of a, U, and L into the supervisory formula gives:

38.This tranche represents a case in which the attachment point A is less than KA but the detachment point D is greater than KA. Thus, according to the Standards, the risk weight for the bank’s exposure is calculated as a weighted average of 12.5 and 12.5×K:

39.With a tranche risk weight of 954%, the bank’s risk-weighted asset amount for this securitisation would be 954% of the 100 million investment, or 954 million. If, for example, the bank chose to apply a capital ratio of 13% to this exposure, then the bank’s required capital would be 13% of 954 million, or approximately 85 million, on the investment of 100 million in this securitisation tranche.

B. External Ratings-Based Approach

40. Consider a non-senior securitisation tranche that has been assigned a rating by one of the eligible rating agencies corresponding to a rating of BB+. Suppose that the tranche has an attachment point A of 5%, a detachment point D of 30%, and effective tranche maturity of MT = 2 years.

• From the look-up table for SEC-ERBA, a non-senior securitisation exposure rated BB+ with one-year maturity has a risk weight of 470%; the risk weight for a five-year maturity is 580%.

• The tranche maturity of 2 years is one-quarter of the way between one year and five years, so the relevant maturity-adjusted risk weight based on linear interpolation is one quarter of the way between 470% and 580%, or 497.5%.

• Because this is a non-senior tranche, it must also be adjusted for tranche thickness, which is the difference between D=30% and A=5%, a difference of 25%. The interpolated risk weight from the table should be multiplied by a factor of 1-(D-A)=0.75, which exceeds the floor of 50% and therefore should be used by the bank in the calculation (0.75 x 497.5%).

• The resulting tranche risk weight is 373%.

41. Banks using the SEC-ERBA for securitisation exposures may prefer to incorporate the main features of the ERBA look-up tables into formal calculations of risk weights, including the relevant adjustments for tranche maturity and tranche thickness. In that case, each pair of 1-year and 5-year risk weights can be viewed as coefficients for a formulaic calculation of the risk weight for a tranche of given maturity MT, and in the case of non-senior tranches, thickness D-A.

42. For example, for a non-senior tranche rated BB+ with MT between one year and five years, the tranche risk weight RWT can be computed with a single formula as:

where the coefficients 4.7 and 5.8 correspond to the relevant values from the look-up table of 470% for one-year maturity and 580% for five-year maturity. Substituting in the values for A, D, and MT from the example above:

43. Senior tranches are not adjusted for thickness; hence, the calculation of the tranche risk weight RWT for a senior BB+ rated tranche would be computed as:

where again the coefficients 1.4 and 1.6 correspond to the relevant values from the senior tranche columns of the look-up table, specifically 140% for 1-year maturity and 160% for 5-year maturity.