Article (5): Liquidity Coverage Ratio (LCR) (Effective Transition From 1 January 2016 for Approved Banks)

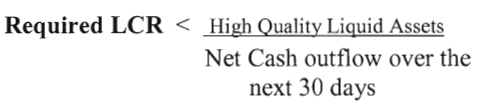

C 33/2015 Effective from 1/1/2016The LCR is taken from Basel III requirements. It represents a 30 day stress scenario with combined assumptions covering both bank specific and market wide stresses that the bank should be able to survive using a stock of high quality liquid assets.

The LCR requires that banks should always be able to cover the net cash outflow with high quality liquid assets.

The Basel III accord requires that the minimum LCR is 100%, starting on 1 January 2015 with 60% minimum coverage and increasing by 10% each year to reach 100% by 1 January 2019.

High quality liquid assets are separated into two categories - Level 1 and Level 2. The composition of Level 1 and Level 2 high quality liquid assets and ‘run off rates’ for cash outflows will be based on the definitions and conditions contained in the document "Basel III: The Liquidity Coverage Ratio and liquidity risk monitoring tools" - issued in January 2013.

The full details of the level 1 and level 2 high quality liquid assets and cash outflows that will apply for the LCR will be contained the Guidance Manual, which is required to be published under Article (10) of these Regulations, taking account of international and local regulatory developments and local market practices.