Standard Re. Regulatory Requirements for Financial Institutions Housing an Islamic Window

N 4743/2020 Effective from 26/10/2020The Central Bank of UAE is pleased to attach herewith the Standard Re. Regulatory Requirements for Financial Institutions Housing an Islamic Window, which applies to licensed financial institutions that conduct part of their activities and businesses in accordance with the provisions of Islamic Shari’ah (Financial Institutions Housing an Islamic Window).

This Standard must be read in conjunction with the regulations, standards and resolutions issued by the Central Bank and the Higher Shari’ah Authority.

This Standard is mandatory and effective from the date of this notice, taking into account what is stated in Article No. (8) of the Standard.

Please bring this Standard to the attention of the board of directors of your institution at the next board meeting.

Article (1) Introduction

- 1.1 The Central Bank seeks to promote the development of banking activities to ensure their effectiveness and efficiency. To achieve this, licensed financial institutions that conduct part of their activities and businesses in accordance with the provisions of Islamic Shari’ah (“Institution housing an Islamic Window”) must establish a framework to ensure that the Shari’ah compliant activities and businesses are conducted in a manner that complies with the requirements set in this Standard and other Regulations and Standards issued by the Central Bank.

- 1.2 This Standard articulates the minimum requirements that Institutions housing an Islamic Window are required to comply with.

- 1.3 This Standard is issued pursuant to the powers vested in the Central Bank under the provisions of the Decretal Federal Law No. (14) of 2018 Regarding the Central Bank & Organization of Financial Institutions and Activities (the Central Bank Law).

- 1.4 Where this Standard specifies requirements to provide information, undertake certain measures, or address certain terms listed as a minimum, the Central Bank may impose requirements which are additional to those outlined in the relevant article.

- 1.1 The Central Bank seeks to promote the development of banking activities to ensure their effectiveness and efficiency. To achieve this, licensed financial institutions that conduct part of their activities and businesses in accordance with the provisions of Islamic Shari’ah (“Institution housing an Islamic Window”) must establish a framework to ensure that the Shari’ah compliant activities and businesses are conducted in a manner that complies with the requirements set in this Standard and other Regulations and Standards issued by the Central Bank.

Article (2) Objective

- 2.1 The objective of this Standard is to establish minimum requirements for the Shari’ah compliant activities and businesses of Institutions housing an Islamic Window, with a view to:

- Ensuring robust governance towards activities and businesses that comply with Islamic Shari’ah, and

- Contributing to financial stability and consumer protection.

- 2.2 This Standard elaborates on the supervisory expectations of the Central Bank with respect to Institutions housing an Islamic Window.

- 2.1 The objective of this Standard is to establish minimum requirements for the Shari’ah compliant activities and businesses of Institutions housing an Islamic Window, with a view to:

Article (3) Scope of Application

- 3.1 This Standard applies to all Institutions housing an Islamic Window. Institutions housing an Islamic Window established in the UAE with Group relationships, including Subsidiaries, Affiliates, or international branches, must ensure that the Standard is adhered to on a solo and Group-wide basis.

- 3.2 This Standard must be read in conjunction with the Standards and Resolutions issued by HSA and notified to Institutions housing an Islamic Window.

- 3.1 This Standard applies to all Institutions housing an Islamic Window. Institutions housing an Islamic Window established in the UAE with Group relationships, including Subsidiaries, Affiliates, or international branches, must ensure that the Standard is adhered to on a solo and Group-wide basis.

Article (4) Definitions

For the purposes of this Standard, the following words and phrases shall have the meanings stated below.

- a. Senior Management: The executive management of the Institution housing an Islamic Window responsible and accountable to the Board for the sound and prudent day-to-day management of the financial institution, generally including, but not limited to, the chief executive officer, chief financial officer, chief risk officer, and heads of the compliance and internal audit functions. The term Senior Management includes the head of Islamic banking at the Institutions housing an Islamic Window.

- b. Independence: Ensuring that the ISSC is not subject to any form of undue influence when issuing resolutions and fatwas in accordance with the Shari’ah parameters, and ensuring that the Internal Shari’ah Control Division or Section and Shari’ah Audit Division or Section are also not subject to any form of undue influence. This should be carried out to strengthen the confidence of both shareholders and stakeholders in the Institution housing an Islamic Window compliance with Islamic Shari’ah.

- c. Internal Shari’ah Audit: regular process to inspect and assess Institution housing an Islamic Window’s compliance with Islamic Shari’ah and the level of adequacy and effectiveness of the Institutions housing an Islamic Window’s Shari’ah governance systems.

- d. Compliance with Islamic Shari’ah refers to compliance with Islamic Shari’ah in accordance with:

a. resolutions, fatwas, regulations, and standards issued by the HSA in relation to licensed activities and businesses of Institutions housing an Islamic Window (“HSA’s Resolutions”), andb. resolutions and fatwas issued by ISSC (“ISSC”) of respective Institution housing an Islamic Window, in relation to licensed activities and businesses of such institution (“the Committee’s Resolutions”), provided they do not contradict HSA’s Resolutions.

- e. Shari’ah Supervision: monitoring of Institution housing an Islamic Window’s compliance with Islamic Shari’ah in all its objectives, activities, operations, and code of conduct.

- f. Subsidiary: An entity, owned by another entity by more than 50% of its capital, or under full control of that entity regarding the appointment of its board of directors.

- g. Affiliate: An entity owned by another entity by more than 25% and less than 50% of its capital.

- h. Fatwas: juristic opinions on any matter pertaining to Shari’ah issues in Islamic finance, issued by HSA or ISSC.

- i. Internal Shari’ah Supervision Division (or Section): a technical division (or section) in the Institution housing an Islamic Window with a mandate to support the ISSC in its mandate.

- j. Internal Shari’ah Supervisory Committee (“ISSC”): a body appointed by the Institution housing an Islamic Window, comprised of scholars specialized in Islamic financial transactions, which independently supervises transactions, activities, and products of the Institution housing an Islamic Window and ensures they are compliant with Islamic Shari’ah in all its relevant objectives, activities, operations, and code of conduct.

- k. Board: Institution housing an Islamic Window’s board of directors.

- l. Group: A group of entities which includes an entity (the ‘first entity’) and:

a. any Controlling Shareholder of the first entity;

b. any Subsidiary of the first entity or of any Controlling Shareholder of the first entity; and

c. any Affiliate, joint venture, sister company and other member of the Group. - m. Shari’ah Non-Compliance Risks: probability of financial loss or reputational risk that an Institution housing an Islamic Window might incur or suffer for not complying with Islamic Shari’ah.

- n. Confidential Information: information that is publicly unavailable and where its disclosure is not allowed as per Article 120 of Decretal Federal Law No. (14) of 2018.

- o. Higher Shari’ah Authority (HSA): is the Central Bank’s Higher Shari’ah Authority for Islamic banking and financial activities.

- p. Islamic Window: refers to the licensed activities that are carried on in accordance with the Islamic Shari’ah that are carried on by financial institutions whether for their account or for the account of or in partnership with third parties which comply with the regulatory requirements stated in this standard and other regulations issued by the central bank.

- q. High Quality Liquid Assets (HQLA): Assets unencumbered by liens and other restrictions on transfer which can be converted into cash easily and immediately, with little or no loss of value, including under the stress scenario.

- a. Senior Management: The executive management of the Institution housing an Islamic Window responsible and accountable to the Board for the sound and prudent day-to-day management of the financial institution, generally including, but not limited to, the chief executive officer, chief financial officer, chief risk officer, and heads of the compliance and internal audit functions. The term Senior Management includes the head of Islamic banking at the Institutions housing an Islamic Window.

Article (5) Governance Requirements

- 5.1 The Institution housing an Islamic Window must comply with Islamic Shari’ah in all of its goals, activities, operations and code of conduct in all matters related to Islamic window at all times.

- 5.2 Branches of foreign licensed financial institutions housing an Islamic Window must adhere to this standard or establish equivalent arrangements to ensure regulatory comparability and consistency. The equivalent arrangement, if applicable, should include the matters related to general assembly, the Board and its Committees without contradicting the prevailing laws in the UAE. The equivalent arrangements shall be submitted to the Central Bank for approval.

- 5.3 Each Institution with an Islamic Window is required to comply with the Shari’ah Governance Standard for Islamic Financial Institutions and other Regulations and Standards issued by the Central Bank, including but not limited to:

- a. The organizational structure of the Islamic window should ensure that the Shari’ah control divisions or sections are independent and are not subject to any influence that may affect their independence;

b. Alignment of the divisions or sections stated in the clause (a) with the three lines of defense approach as set out in the Central Bank’s Corporate Governance Standard and Shari’ah Governance Standard for Islamic financial institutions.

5.4 The Board is in ultimate control of the Institution housing an Islamic Window and accordingly responsible for the Islamic Window’s compliance with Islamic Shari’ah and the requirements set in this Standard.

5.5 Senior Management of the Institution with an Islamic Window is responsible and accountable to the Board for the sound and prudent day-to-day management of the Institution including executing and managing the Shari’ah compliant activities and businesses. All the Shari’ah compliant activities and business of the Institution must be offered through the Islamic window.

5.6 The Institution housing an Islamic Window should appoint a Head of Islamic Window who must be dedicated to the operations of the Islamic Window and must not perform any tasks that are not within the scope of the Islamic Window.

5.7 The appointment of the Head of Islamic Window must be approved by the Central Bank. The Central Bank must be informed regarding the organizational structure of the Islamic Window at least 20 working days before the same is implemented.

5.8 The Head of Islamic Window should report directly to the Executive Management Committee of the Institution or the CEO. The Head of Islamic Window is responsible and accountable to the Executive Management Committee of the Institution or the CEO for the operations of Shari’ah compliant activities and businesses. The Head of the Islamic Window is responsible to coordinate with the relevant departments concerning activities and businesses that comply with Islamic Shari’ah and shall be regarded part of the business line.

5.9 The Head of Islamic Window should:- have a bachelor degree or masters in banking and finance or other relevant fields,

- demonstrate adequate knowledge, and experience (not less than 10 years) in Islamic banking and finance that will allow him/her to lead Shari’ah compliant business, and

- have held relevant senior positions in the banking sector or other relevant sectors.

9.5 The Institution housing an Islamic Window must adopt an approach with regard to conducting the Shari’ah compliant businesses and activities within the institution. Such approach should take into consideration staffing and physical premises in accordance with the size and the complexity of the Shari’ah compliant business and activities. The approach may take one of the following forms:- -Stand-alone separate branches and offices to service the Islamic Banking clientele as well as designated staff;

- -Embedding of designated and/or dedicated Islamic Window personnel within the existing branch network and premises.

- -Any other form subject to the Central Bank approval.

Such approach must be approved by the ISSC and the approach submitted to the Central Bank for review and approval every 5 years unless the HSA or the Central Bank requires a shorter period.

- 5.10 The Institution Housing an Islamic Window may leverage on its existing infrastructure to source Shari’ah compliant activities, including the offering of Shari’ah compliant products and services through the existing business lines. The institution housing an Islamic Window must develop an approach to internal services (between different departments) with respect to Islamic Window in order to ensure the compliance with Islamic Shari’ah at all times.

- 5.11 The approach to internal services must include the following:

- a. A minimum of one designated function to manage Shari’ah compliant Asset and Liability Management (ALM), Treasury and Investment operations.

- b. A dedicated sales function with appropriate Shari’ah qualification to market and sell Shari’ah compliant products and services, and employees at this function are not allowed to market or sell conventional products. Other sales personnel may sell Shari’ah compliant financial products and services to customers provided that they have been given adequate and appropriate training and they are supported by the dedicated Islamic Window sales function.

- c. Development and delivery of a comprehensive and specific training plan to cover all staff engaged in Shari’ah compliant operations, including staff assuming positions in the front line, middle and back offices and control functions, to ensure adequate management of the Shari’ah compliant products and services within the institution. The training program should take into account:

- specifics of the functions (roles) performed by the staff, and equip the staff with information and skills, depending on the nature of work of each employee, to ascertain compliance with Islamic Shari’ah, and

- the general banking and business risks associated and encountered with that function as well as any Shari’ah non-compliance risks.

- d. The approach towards internal services should be approved by the ISSC and submitted to the Central Bank for review and approval. Any material changes thereafter must be submitted to the Central Bank for approval.

- 5.1 The Institution housing an Islamic Window must comply with Islamic Shari’ah in all of its goals, activities, operations and code of conduct in all matters related to Islamic window at all times.

Article (6) Asset and Liability Management

- 6.1 The institution housing an Islamic Window must establish an ALM Framework for the management of Shari’ah compliant assets and liabilities to ensure their sound and prudent management, including ring-fencing of Shari’ah compliant assets and liabilities.

- 6.2 The framework should demonstrate the segregation between Shari’ah compliant assets and liabilities and other assets and liabilities of the Institution.

- 6.3 The segregation must include having separate product codes for Shari’ah compliant products mapped with specific General Ledger accounts. Institution housing an Islamic Window may apply alternative methods, subject to the approval of the Central Bank.

- 6.4 The Institution housing an Islamic Window is required to report a separate Liquidity Coverage Ratio (LCR)/Net Stable Funding Ratio (NSFR)/Eligible Liquid Assets Ratio (ELAR) (as applicable) for the Islamic Window. These reports are to be submitted along with periodic reports submitted to the Central Bank.

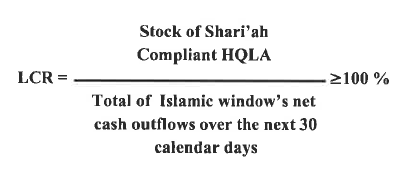

- 6.5 If the Institution housing an Islamic Window is maintaining separate liquidity levels for the Islamic Window, an appropriate stock of Shari’ah compliant High Quality Liquid Assets must be held against 30 days net outflow and documented accordingly for Central Bank supervision and examination review. Documentation must be retained for two years from any point in time that the information is documented

- 6.6 The formula of calculating LCR, specific to the Islamic Window operation is as follows:

6.7 Any surplus or deficit in Shari’ah compliant assets and liabilities in the Islamic Window must be managed in a Shari’ah compliant manner. Institutions must develop an approach to the mechanism of financing and funding between the Islamic window and the institution. The approach developed must be reviewed and approved by the ISSC and the Central Bank.

6.7 Any surplus or deficit in Shari’ah compliant assets and liabilities in the Islamic Window must be managed in a Shari’ah compliant manner. Institutions must develop an approach to the mechanism of financing and funding between the Islamic window and the institution. The approach developed must be reviewed and approved by the ISSC and the Central Bank.- 6.8 The management and treatment of non-Shari’ah compliant income shall be carried out in accordance with the directives of the ISSC.

- 6.9 Non-Shari’ah compliant income, if any, must be treated in accordance with the Shari’ah requirements in this regard.

- 6.10 There should be no internal procedure or a policy that encourages converting Shari’ah compliant assets to conventional assets. Similarly, the institution housing an Islamic Window must not transfer Shari’ah compliant assets (which are in the Islamic Window) to its conventional side in order to deal with it as a conventional asset. The Senior Management should ensure the independence of the Shari’ah compliance businesses and activities, and Islamic Window’s customers from the conventional businesses and activities.

- 6.11 All marketing and promotional material of Shari’ah compliant activities of the Bank must be formulated under a separate brand (e.g. different logo and different commercial name) and must be approved by the ISSC.

- 6.1 The institution housing an Islamic Window must establish an ALM Framework for the management of Shari’ah compliant assets and liabilities to ensure their sound and prudent management, including ring-fencing of Shari’ah compliant assets and liabilities.

Article (7) Regulatory and Financial Reporting, IT Systems and Infrastructure

- 7.1 The Institutions housing an Islamic Window are mandated to report a separate Islamic Bank Return Form “iBRF” as per the template set out by the Central Bank.

- 7.2 The Institutions housing an Islamic Window are required to separately report the results and activities of their Islamic Window to Executive Management and the Board. Such internal reporting shall include among other items an appropriate allocation of the costs of internal services to accurately reflect the cost of offering Shari’ah compliant financial services.

- 7.3 The reports produced by the Shari’ah control department or division and by the Shari’ah Audit department or division should be submitted in accordance with the requirements stated in the Shari’ah Governance Standard for Islamic Financial Institution.

- 7.4 The institution housing an Islamic Window are encouraged to separately report the results and activities of their Islamic Window operations within the annual report to promote market disclosure, transparency and customer confidence.

- 7.5The institution housing an Islamic Window may use a single or dual core banking system to record, manage and report Shari’ah compliant activities and other activities.

- 7.6 Where a single core banking system is used, it must be adjusted to account for the unique features of Shari’ah compliant products. Such adjustments for Shari’ah compliance purposes must be approved by the ISSC.

- 7.1 The Institutions housing an Islamic Window are mandated to report a separate Islamic Bank Return Form “iBRF” as per the template set out by the Central Bank.

Article (8) Compliance with the Standard

- 8.1 The Institutions housing an Islamic Window must set a Shari’ah governance framework in accordance with this Standard within 180 days from issuing this standard. The same must be submitted to the Central Bank for approval.

- 8.2 The Institutions housing an Islamic Window should comply fully with these standard requirements within one year from publishing this standard.

- 8.3 The Regulatory Development Division of the Central bank shall be the reference for interpretation of the provisions of this Standard.

- 8.1 The Institutions housing an Islamic Window must set a Shari’ah governance framework in accordance with this Standard within 180 days from issuing this standard. The same must be submitted to the Central Bank for approval.