6.1 The institution housing an Islamic Window must establish an ALM Framework for the management of Shari’ah compliant assets and liabilities to ensure their sound and prudent management, including ring-fencing of Shari’ah compliant assets and liabilities.

6.2 The framework should demonstrate the segregation between Shari’ah compliant assets and liabilities and other assets and liabilities of the Institution.

6.3 The segregation must include having separate product codes for Shari’ah compliant products mapped with specific General Ledger accounts. Institution housing an Islamic Window may apply alternative methods, subject to the approval of the Central Bank.

6.4 The Institution housing an Islamic Window is required to report a separate Liquidity Coverage Ratio (LCR)/Net Stable Funding Ratio (NSFR)/Eligible Liquid Assets Ratio (ELAR) (as applicable) for the Islamic Window. These reports are to be submitted along with periodic reports submitted to the Central Bank.

6.5 If the Institution housing an Islamic Window is maintaining separate liquidity levels for the Islamic Window, an appropriate stock of Shari’ah compliant High Quality Liquid Assets must be held against 30 days net outflow and documented accordingly for Central Bank supervision and examination review. Documentation must be retained for two years from any point in time that the information is documented

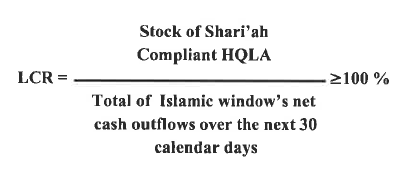

6.6 The formula of calculating LCR, specific to the Islamic Window operation is as follows:

6.7 Any surplus or deficit in Shari’ah compliant assets and liabilities in the Islamic Window must be managed in a Shari’ah compliant manner. Institutions must develop an approach to the mechanism of financing and funding between the Islamic window and the institution. The approach developed must be reviewed and approved by the ISSC and the Central Bank.

6.8 The management and treatment of non-Shari’ah compliant income shall be carried out in accordance with the directives of the ISSC.

6.9 Non-Shari’ah compliant income, if any, must be treated in accordance with the Shari’ah requirements in this regard.

6.10 There should be no internal procedure or a policy that encourages converting Shari’ah compliant assets to conventional assets. Similarly, the institution housing an Islamic Window must not transfer Shari’ah compliant assets (which are in the Islamic Window) to its conventional side in order to deal with it as a conventional asset. The Senior Management should ensure the independence of the Shari’ah compliance businesses and activities, and Islamic Window’s customers from the conventional businesses and activities.

6.11 All marketing and promotional material of Shari’ah compliant activities of the Bank must be formulated under a separate brand (e.g. different logo and different commercial name) and must be approved by the ISSC.

6.7 Any surplus or deficit in Shari’ah compliant assets and liabilities in the Islamic Window must be managed in a Shari’ah compliant manner. Institutions must develop an approach to the mechanism of financing and funding between the Islamic window and the institution. The approach developed must be reviewed and approved by the ISSC and the Central Bank.

6.7 Any surplus or deficit in Shari’ah compliant assets and liabilities in the Islamic Window must be managed in a Shari’ah compliant manner. Institutions must develop an approach to the mechanism of financing and funding between the Islamic window and the institution. The approach developed must be reviewed and approved by the ISSC and the Central Bank.